Personal

Deposit Account

Agreement

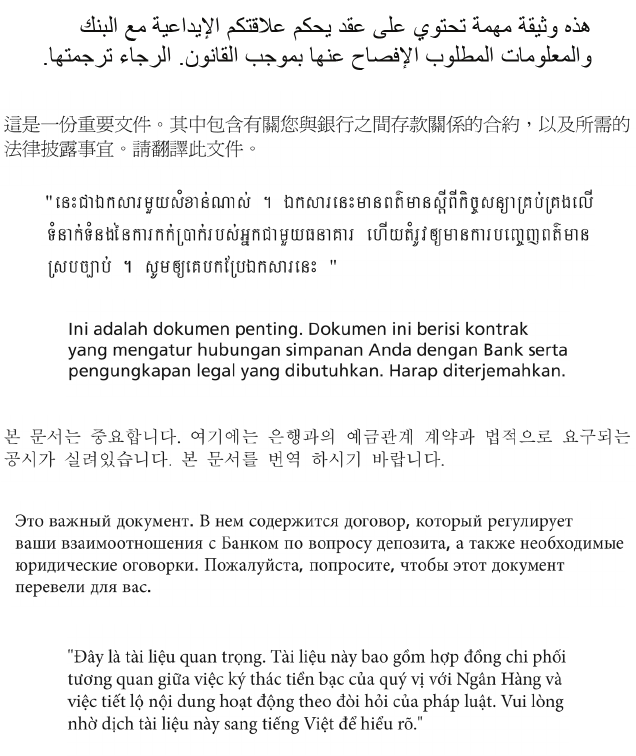

This is an important document. It contains the contract governing your deposit relationship with

the Bank and required legal disclosures. Please have it translated.

E

ste es un documento importante. Contiene el contrato que rige su relación de depósitos con el

Banco y declaraciones de información exigidas por ley. Por favor, mande a hacer la traducción

de este documento.

C

e document est important. Il contient le contrat régissant vos rapports avec la Banque en votre

qualité de déposant ainsi que les informations exigées par la loi. Veuillez le faire traduire.

Este documento é importante. Contém o contrato que governa a sua relação para depósitos com

o banco e as declarações requeridas por lei. Por favor mande traduzir.

ั

่

้

Language Practices at TD Bank

Thank you for banking with us. Please be aware that verbal and written communications from TD Bank ordinarily will be in English. These

communications in English may include, but are not limited to, applications, account agreements, statements and disclosures, notices concerning

changes in terms or fees, and communications related to account servicing. As a courtesy to our customers, we sometimes communicate in

languages other than English. If you need assistance in a language other than English, please contact us, as we have language services that may

help. However, we cannot guarantee that customer service or other Bank communications will be available in any language other than English,

and many important bank documents are available only in English.

Gracias por realizar sus operaciones bancarias con nosotros. Tenga en cuenta que las comunicaciones verbales y escritas de TD Bank

normalmente estarán en inglés. Estas comunicaciones en inglés pueden incluir, entre otras, solicitudes, acuerdos de cuenta, estados de

cuenta y divulgaciones, avisos relacionados con cambios en los términos o cargos, y comunicaciones relacionadas con la administración de

cuentas. Como cortesía hacia nuestros clientes, a veces nos comunicamos en otros idiomas que no sean el inglés. Si necesita asistencia en

otro idioma que no sea inglés, comuníquese con nosotros, ya que contamos con servicios lingüísticos que pueden ayudar. Sin embargo, no

podemos garantizar que el servicio al cliente u otras comunicaciones del banco estarán disponibles en otro idioma que no sea inglés, y muchos

documentos bancarios importantes están disponibles solo en inglés.

Mèsi poutèt ou chwazi nou pou zafè labank ou. Tanpri, se pou ou konnen kominikasyon aloral ak alekri ki soti nan TD Bank òdinèman se an Anglè

yo pral ye. Kominikasyon an Anglè sa yo ka gen ladan, men se pa sa sèlman, aplikasyon yo, akò kont yo, relve ak deklarasyon yo, avi konsènan

chanjman nan kondisyon yo oswa frè yo, epi kominikasyon anrapò ak jesyon kont lan. Kòm yon koutwazi nou fè kliyan nou yo, pafwa nou

kominike nan lòt lang ki pa Anglè. Si ou bezwen èd nan yon lòt lang ki pa Anglè, tanpri kontakte nou, paske nou gen sèvis lang ki gendwa ede

ou. Sepandan, nou pa kapab garanti ke sèvis kliyan an oswa lòt kominikasyon Labank yo pral disponib nan okenn lòt lang ki pa Anglè, epi anpil

dokiman labank enpòtan yo disponib an Anglè sèlman.

Obrigado por utilizar nossos serviços bancários. Saiba que os comunicados verbais e escritos do TD Bank normalmente estarão em inglês. Esses

comunicados em inglês podem incluir, entre outros assuntos, requisições, contratos de conta, extratos e divulgações, avisos sobre alterações em

termos ou taxas, e comunicações relacionadas com os serviços da conta. Como cortesia a nossos clientes, nós nos comunicamos algumas vezes

em outros idiomas. Caso você precise de assistência em um idioma diferente do inglês, entre em contato conosco para que possamos ajudar. No

entanto, não podemos assegurar que o atendimento ao cliente ou outros comunicados do Banco estejam disponíveis em qualquer idioma além

do inglês, e muitos documentos importantes do banco estão disponíveis apenas em inglês.

شكراً لكم على اختيارنا لإجراء تعاملاتكم المصرفية. يُ رجى العلم أن المراسلات الشفوية والكتابية الصادر نTD Bank ستكون عادةً باللغة الإنجليزية. قد تشمل هذه

المراسلات باللغة الإنجليزية، على سبيل المثال لا الحصر، الطلبات، واتفاقيات الحسابات، والبيانات والإفصاحات، والإخطارات بشأن تغييرات في الشروط أو الرسوم،

والمراسلات المتعلقة بخدمة الحسابات. إلّ ا أننا نعمد أحياناً إلى إصدار مراسلاتنا بلغات أخرى غير اللغة الإنجليزية على سبيل المجاملة لعملائنا. يُ رجى التواصل معنا إذا

كنتم بحاجة إلى مساعدة بلغة أخرى غير اللغة الإنجليزية لأننا خصصنا خدمات لغوية قد تساعدنا على فهم احتياجاتكم. ومع ذلك، ليس بمقدورنا أن نضمن توفر خدمة العملاء

أو المراسلات الأخرى الصادرة عن البنك بأي لغة أخرى غير اللغة الإنجليزية، كما أن الكثير من الوثائق المصرفية المهمة لن تكون متاحة سوى باللغة الإنجليزية.

感謝您選擇我們銀行。請注意,TD Bank 的口頭及書面通訊通常將以英語進行。這些英語通訊可能包括但不限於申請、帳戶合約、聲明和揭露、條款或費用

變更通知,以及與帳戶服務相關的通訊。基於對顧客的禮貌,我們有時會使用英語以外的語言進行溝通。如果您需要英語以外語言的協助,請聯絡我們,因

為我們有可能對您有幫助的語言服務。然而,我們無法保證客服或其他銀行通訊將以英語以外的任何語言提供,且許多重要的銀行文件僅提供英語版本。

ขอขอบคณททาธรกรรมธนาคารกบเรา โปรดทราบวาการสอสารดวยวาจาและลายลกษณอกษรจาก TD Bank มกจะเปนภาษาองกฤษ การสอสารในภาษาองกฤษอาจรวมถึ งแตไมจากด

เฉพาะการสมคร ขอตกลงบญช คาชแจง และการเปดเผยขอมล ประกาศเกยวกบการเปลยนแปลงขอกาหนดหรอคาธรรมเนยม และการสอสารทเกยวของกบการใหบรการบญช เพ่อความ

สะดวกของลกคาของเรา บางครงเราจึ งสอสารในภาษาอนทไมใชภาษาองกฤษ หากทานตองการความชวยเหลอในภาษาอนทไมใชภาษาองกฤษ โปรดตดตอเรา เนองจากเรามบรการด้าน

ภาษาทอาจชวยได อยางไรกตาม เราไมสามารถรบประกนไดวาฝายบรการลกคาหรอการสอสารอน ๆ ของธนาคารจะใหบรการในภาษาอนทไมใชภาษาองกฤษ และไมสามารถรบประกนไดวา

เอกสารธนาคารทสาคญจานวนมากมเฉพาะภาษาองกฤษเทานน

Terima kasih telah bertransaksi bersama kami. Perlu diketahui bahwa komunikasi lisan maupun tulisan dari Bank TD biasanya akan menggunakan

Bahasa Inggris. Komunikasi dalam bahasa Inggris ini dapat mencakup, namun tidak terbatas pada, pendaftaran, persetujuan rekening,

pernyataan dan pengungkapan, pemberitahuan tentang perubahan persyaratan atau biaya, dan komunikasi yang terkait dengan layanan

pada akun. Sebagai rasa hormat kepada pelanggan kami, terkadang kami berkomunikasi dalam bahasa selain Bahasa Inggris. Jika Anda

membutuhkan bantuan dalam bahasa lain selain Bahasa Inggris, silakan hubungi kami, kami mungkin dapat membantu Anda dengan layanan

bahasa lainnya. Namun, kami tidak menjamin dukungan pelanggan atau komunikasi bank lainnya akan tersedia dalam bahasa lain selain

Bahasa Inggris, dan banyak dokumen bank hanya tersedia dalam Bahasa Inggris.

TD Bank

Благодарим Вас за сотрудничество с нами. Обращаем Ваше внимание на то, что устные и письменные сообщения от TD Bank обычно будут на английском

языке. Эти сообщения на английском языке могут включать, помимо прочего, следующее: заявки, соглашения о счетах, финансовая отчетность и раскрытие

информации, уведомления об изменениях в условиях или платежах, а также сообщения, связанные с обслуживанием счета. В знак уважения к нашим клиентам

мы иногда ведем переписку не на английском языке. Если Вам нужна помощь на другом языке (не на английском), пожалуйста, свяжитесь с нами, поскольку

у нас есть отдел лингвистических услуг, который может помочь. Тем не менее, мы не можем гарантировать, что клиентская служба или другие банковские

сообщения будут доступны на каком-либо языке, кроме английского, и многие важные банковские документы доступны только на английском языке.

Cảm ơn quý khách đã sử dụng dịch vụ ngân hàng của chúng tôi. Xin lưu ý rằng thông tin liên lạc bằng lời và bằng văn bản từ Ngân hàng TD theo cách

thông thường sẽ bằng tiếng Anh. Những thông tin liên lạc bằng tiếng Anh này có thể bao gồm, nhưng không giới hạn ở, các đơn đăng ký, thỏa thuận tài

khoản, sao kê và tiết lộ, thông báo liên quan đến những thay đổi về các điều khoản hoặc phí và thông tin liên quan đến dịch vụ tài khoản. Như một phép lịch

sự với khách hàng, đôi khi chúng tôi giao tiếp bằng các ngôn ngữ khác ngoài tiếng Anh. Nếu quý khách cần hỗ trợ bằng ngôn ngữ khác ngoài tiếng Anh, vui

lòng liên hệ với chúng tôi, vì chúng tôi có các dịch vụ ngôn ngữ có thể trợ giúp quý khách. Tuy nhiên, chúng tôi không thể đảm bảo rằng dịch vụ khách hàng

hoặc thông tin liên lạc khác của Ngân hàng sẽ được cung cấp bằng bất kỳ ngôn ngữ nào khác ngoài tiếng Anh và nhiều tài liệu ngân hàng quan trọng chỉ có

bằng tiếng Anh.

1

.............................................................................................

...............................

........................................................................................

..................................................................................................

.....................................................

...............................................................................

................................................................................

...........................................................

....................................

...................................................................................

..........................................................................

............................................................................................

.....................................................................................

.........................................

..............................

.................................................

..........................

..............................................................................

..............................................................................

..............................................................................

..........................................

.....................................................................

..............................................................................

.....................................................................................

.................................

................................................................................

.......................................................................

..........................................................................

...........................................................

......................................................................

.....................................

..........................................................................

...................................................................................

.........................................................................

...................................................................................

..................................................................................................

.............................................................................................

...................................................................................

..................................

......................................................................................

..............................................................................

.......................................................

...................................................................................

......................................

.....................................................

..........................................................

......................................................

............................................................

................................

..........................................

...............................................................

........................................................

...................................................................

.......................................................................................

.........................................................................

.....................................................................................

....................................................................................

...............................................................

...........................................................................

...........................................................

.................................................................................................

...............................................................

................................................

.......................................................................

...................................................

....................................................

.....................................................

.........................................................................................

............................................

....................................................................

.......................................................................

...................................................................................

..........................................................................

...............................

...............................................................

..............

.......................................................................

.................................................................................

........................

......................................................................

.....................

..............................................................

.........................

...............................................

.........................................................................

.............................................................................

...................................................................

............................................................................

.................................................................................

.........................................................................

..........................................................................

.................................................................

........................................................................................

......................

...........................................................

........................

Welcome to TD Bank, America’s Most Convenient Bank

®

We are pleased to offer you this Personal Deposit Account Agreement (“Agreement”) that governs the terms and conditions of your personal deposit

Account(s) with us. This Agreement consists of Parts IVI below, any supplement(s) and amendment(s), as well as the Deposit Rate Sheet(s), Personal Fee

Schedule(s) and Account Maintenance Information grid(s) published by the Bank from time to time. This Agreement provides you with information you

will want to know about your personal deposit Account(s). If you have any questions, or would like to learn more about our personal deposit Account

products and services, please contact any of our Stores or call us at 18887519000

. We will be happy to assist you.

P

art I: Terms and Conditions

Deinitions 2

Personal Depo

sit Account Terms and Conditions 2

Deposit Policy 2

Checks 3

Returned Checks/Waiver of Rights 3

Cashing of Checks 3

Withdrawal Policy 3

Processing Order for Payment of Checks, Debit Card

Transactions, and Other Items 3

Reasons Why We May Refuse to Pay an Item 4

Postdated Items 4

Pre-authorized Drafts 4

Overdrafts 5

Stop Payments 6

International, ACH, The Clearing House Real-Time

Payments (“TCH RTP”) and Wire Transfers 6

Periodic Statements; Time Limit to Report Errors 6

Combined Statements with Checking 7

Important Information for Opening a New Account 7

Telephone Numbers 7

Account Ownership 7

Individual Accounts 7

Joint Accounts–With Right of Survivorship 7

No Two-Signer Accounts 8

Specialty Accounts 8

Trust Accounts 8

Uniform Gifts/Transfers To Minors Act Account 8

Power of Attorney 8

Certiied Taxpayer Identiication Number or

Social Security Number 8

Credit Veriication and Obtaining

Financial Information 9

Conlicting Demands/Disputes 9

Changing Your Account 9

Adverse Claims; Interpleader; Legal Process 9

If You Owe Us Money 10

Right of Set-Off 10

Death/Incompetence 10

Limited Liability 10

Default 11

Indemnity 11

Jury Trial Waiver 11

Demand Deposit Accounts and Sub-Accounts 11

Miscellaneous 11

Part II: Truth in Savings Disclosure

Accounts Covered 13

Minimum Account Requirements 13

Fees & Charges 13

Interest Rate and Annual Percentage Yield 13

Checking Balance Tier Structures 13

Checking Account Information 13

Savings Balance Tiers Structures 14

Savings Account Information 14

Special Information for Certiicates of Deposit 15

Part III: Funds Availability Policy

Determining the Availability of a Deposit 16

Standard Funds Availability 17

Special Rules for New Accounts 17

Longer Delays May Apply 17

TD FastFunds 17

Holds on Other Funds 17

Non-U.S. Financial Institutions 17

Returned Items Subsequent to Availability of Funds 18

Endorsements 18

Part IV: Electronic Funds Transfers Disclosure

Direct Deposits 18

Pre-authoriz

ed Withdrawals 18

Telephone Transfers 18

Electronic Check Conversions 18

Bill Pay 18

External Transfer (Account to Account Transfers) Service

and Send Money with Zelle

®

18

Personal Identiication Number (PIN) 19

ATM Transaction Types 19

Visa

®

Debit Card Transaction Types 19

Customer Safety Information – NY 19

Customer Safety Information – NJ 19

Termination 19

Charges For Electronic Funds

Transfers 19

Right to Documentation 20

Terminal Transactions 20

Direct Deposits 20

Periodic Statements 20

Passbook Accounts Where the Only Possible

Electronic Funds Transfers Are Direct Deposits 20

Notice of Varying Amounts 20

Pre-authorized (Recurring) Transfers and Stop Payments 20

Additional Information Required

By Massachusetts Law 21

EFT: Our Liability 21

Disclosures of Account Information to Third Parties 21

Unauthorized Transfers 21

Errors or Questions About Electronic Funds Transfers 22

Part V: Substitute Checks and Your Rights

What is a Substitute Check? 22

What are my Rights Regarding Substitute Checks? 22

How do I Make a Claim for a Refund? 22

Part VI: Night Depository Agreement

Bags and Containers 23

Method of Deposit 23

Receipt of Bag and Keys 23

Third Party Carriers 23

Liability of Bank 23

Contents Not Insured 23

Processing Deposits 23

Fees and Service Charges 23

Termination 23

Entire Agreement; Conlict of Terms: Governing Law 23

2

Deinitions

Throughout this Agreement, unless otherwise indicated, the following words have the meanings given to them below:

a

) “Account” means your Checking Account, Money Market Account, personal CD Account and/or Savings Account with us, including Individual

Retirement Accounts (IRAs), as applicable, unless limited by the heading under which it appears.

b

) “TD Essential Banking Account” is a Checking Account without check writing privileges. TD will not issue checks and may choose not to honor

checks written on this Account.

c) “Business Day” means every day, except Saturdays, Sundays, and federal holidays.

d) “Calendar Day” means every day, including Saturdays, Sundays, and federal holidays.

e) “Bank,” “we,” “us,” “our” and “TD Bank” refer to TD Bank, N.A.

f) “You” and “your” mean each depositor who opens an Account, and any joint owner of each Account.

g) “Store” means a branch ofice.

Part I: Personal Deposit Account Terms and Conditions

By opening and maintaining an Account with the Bank, you agree to the provisions of this Agreement. You should read this Agreement thoroughly

and keep it with other important records. From time to time, we may offer new types of Accounts and may cease offering some types of Accounts.

This Agreement governs all of these new types of Accounts, and continues to govern any Accounts you may have that we no longer offer. If and

to the extent the provisions of this Agreement vary from the provisions of the Uniform Commercial Code as adopted in the jurisdiction where your

Account was opened, the terms and conditions of this Agreement shall control.

This Agreement includes your promise to pay the charges listed on the Personal Fee Schedule and Account Maintenance Information grid

and your permission for us to deduct these charges, as earned, directly from your Account. You also agree to pay any additional reasonable

charges we may impose for services you request which are not contemplated by this Agreement but are disclosed in our Personal Fee Schedule,

which may be amended from time to time. Each of you agree to be jointly and severally liable for any Account deicit resulting from charges or

overdrafts, whether caused by you or another authorized to withdraw from your Account, together with the costs we incur to collect the deicit,

including, to the extent permitted by law, our reasonable attorneys’ fees.

You agree to use the Account only for lawful purposes, and you acknowledge and agree that “restricted transactions” as deined in the Unlawful

Internet Gambling Enforcement Act of 2006 and Regulation GG issued thereunder are prohibited from being processed through your Account

or any relationship between you and the Bank. In the event we identify a suspected restricted transaction, we may block or otherwise prevent

or prohibit such transaction; and further, we may deny services to you, close the Account, or end the relationship. However, in the event that a

charge or transaction described in this disclosure is approved and processed, you will still be liable for the charge. In order to protect you, we may

ask for identiication or may ask identifying questions to authenticate you prior to processing a request or transaction.

Deposit Policy

We may refuse to accept an item for deposit or to return all or a part of it to you. Any item that we accept for deposit is subject to later veriication.

We will usually give you provisional credit for items deposited into your Account. However, we may delay or refuse to give you provisional credit

if we believe in our discretion that your item will not be paid. We will reverse any provisional credit we have given for an item deposited into your

Account if we do not receive inal credit for that item, and charge you a fee (see Personal Fee Schedule). If the reversal of a provisional credit

creates an overdraft in your Account, you will owe us the amount of the overdraft, plus any overdraft fees when applicable (see Personal Fee

Schedule). We will determine when inal credit is received for any item. Please read the Funds Availability Policy for a detailed discussion of how

and when we make funds available to you.

We will accept certain items like foreign checks and bond coupons for collection only. You may also ask us to accept certain other items for

collection only. You will not receive credit for (provisional or otherwise), and may not withdraw funds against, any of these items until we receive

inal credit from the person responsible for paying them. Items sent for collection will be credited to your Account in U.S. dollars, calculated using

our applicable exchange rate that is in effect on the date when we credit the funds to your Account and not when the deposit is made. We may

earn revenue on this exchange. The Funds Availability Policy does not apply to items we have accepted for collection only. If and when we receive

inal credit for an item we have accepted for collection only, you agree that we may subtract our collection fee (see Personal Fee Schedule) from

the amount inally credited to us, before we credit your Account for the remaining amount.

For certain eligible direct deposits, we may make funds available for your use up to two days before we receive the funds from your payor with

our service, TD Early Pay. There is no enrollment necessary and no fee for this service. Not all direct deposits are eligible for TD Early Pay. Eligible

direct deposits are limited to electronic direct deposits such as your payroll, pension, and government beneit payments. Other deposits or credits

to your account, such as deposits of funds from person-to-person payments services (e.g., Zelle®), check or mobile deposits, and other online

transfers are not eligible for TD Early Pay. The Bank does not guarantee that any direct deposits will be made available before the date scheduled

by the payor, and early availability of funds may vary between direct deposits from the same payor.

When funds are made available early, they will be relected in your account’s available balance. Whether we make funds available early depends

on (1) when we receive the payor’s payment instructions, (2) any limitations we set on the amount and frequency of early availability, and (3)

standard fraud prevention screening.

If a direct deposit is not made available early, it will be made available in accordance with our Availability of Funds Policy described in this

Agreement. Except as expressly set forth herein, funds made available early are subject to the same terms and conditions as other deposits

to your account. If we’ve made funds available early and the payor reverses or requests a return of the deposit, or the funds are otherwise

uncollected by the Bank, you understand and agree that we may debit your account in accordance with our normal process found in subpart

e) Direct Deposits, found in this Agreement, up to the amount of the deposit that was previously made available – even if you have already

withdrawn the funds or it creates an overdraft on your account, without prior notice from us and at any time. In this instance, you are responsible

for any fees assessed – including those charged by merchants or third parties – as a result of the overdraft. TD Early Pay is offered at the discretion

of the Bank, and we reserve the right to cancel the service at any time and without notice to you.

3

C

hecks

All negotiable paper (called “checks”) presented for payment must be in a form supplied by or previously approved by the Bank. The Bank may

refuse to accept any check that does not meet this requirement or which is incompletely or defectively drawn. Once an outstanding check is six

(6) months old, we may elect not to pay it. But if there is no stop payment order on ile when we receive the check for payment, we may elect to

pay it in good faith without consulting you. You agree that you will use care in safeguarding your unsigned checks against loss or theft. You will tell

us immediately if any checks are missing. You agree to assume all losses that could have been prevented if you had safeguarded unsigned

(or otherwise incomplete) checks, or had told us they were missing.

Returned Checks/Waiver of Rights

If you deposit a check or item in your Account that the drawee bank returns unpaid for any reason (called “dishonor”), the amount of the

dishonored check or item will be deducted from your Account. We may put the dishonored check or item through for collection again. This

means that you are waiving your right to receive immediate notice of dishonor. The Bank may also collect any amounts due to the Bank

because of returned checks, through the right of set-off, from any other of your Accounts at the Bank, or collect the funds directly from you.

Cashing of Checks

Typically, the Bank will cash checks drawn on other banks for its Customers who have adequate available funds in their Account(s). If any such

check should be returned by the paying bank for any reason, the Bank will charge you a fee (see Personal Fee Schedule). In addition, the Bank will

debit the amount of the returned check from your Account(s). If the debit creates an overdraft in your Account, you will owe us the amount of the

overdraft plus any overdraft fees when applicable (see Personal Fee Schedule).

Withdrawal Policy

Passbook Account (if avai

lable in your jurisdiction) withdrawals can be made by an authorized signer only upon presentation of the passbook,

either in person or accompanied by a written order of withdrawal. If you lose the passbook, we require that a Lost Passbook Afidavit be signed by

ALL persons named on the Account before a notary public.

S

tatement Savings Account withdrawals can be made per written order of withdrawal in accordance with the information contained on the

signature card and may also be made with an ATM or Visa® Debit Card, as applicable. The Bank may refuse a request if any document or

identiication required by the Bank or law in connection with the withdrawal has not been presented.

The Bank reserves the right to require seven (7) Calendar Days written notice prior to withdrawal or transfer of funds from all Savings or Money

Market Accounts offered by the Bank.

For any non-transactional savings Account(s), and money market Account(s), you may make as many in-person withdrawals at a teller window or

any ATM as you wish. However, our bank policy allows no more than a combined total of six (6) pre-authorized, automatic, electronic (including

computer or mobile initiated), or telephone withdrawals or transfers, or payments by check, draft, debit card, or similar order payable to third

parties or made payable to yourself in any monthly period (based on your statement date). We may impose a fee, as disclosed on the Personal Fee

Schedule, for the seventh (7th) withdrawal, and each additional withdrawal that you make in any monthly period (based on your statement date).

These fees will be relected in your monthly statement.

For Holiday Club and Club Saver Accounts, we may impose a fee, as disclosed on the Personal Fee Schedule, for the fourth (4th) withdrawal, and

each additional withdrawal that you make in any calendar month.

Processing Order for Payment of Checks, Debit Card Transactions, and Other Items

The following describes how we pay or charge to your Account checks, debit card transactions, and other items presented for payment or

deposit. An “item” includes any instruction or order for the payment, transfer, deposit, or withdrawal of funds, including, but not limited to,

any check, substitute check, purported substitute check, remotely created check or draft, electronic transaction, draft, demand draft, image

replacement document, indemniied copy, ATM withdrawal or transfer, debit card point-of-sale transaction, pre-authorized debit card payment,

automatic transfer, telephone-initiated transfer, ACH transaction, online banking transfer to or from Accounts at TD Bank or external transfers to

other institutions, online bill payment instruction, payment to or from other people (Send Money with Zelle

®

transaction), withdrawal or deposit

slip, in-person transfer or withdrawal, cash ticket, deposit adjustment, or wire transfer. In the event that there are insuficient funds in your Account

to pay an item and the transaction is resubmitted, each resubmission constitutes a separate item.

For purposes of determining your available Account balance and processing items to your Account, including returning items due to insuficient

funds or paying items that overdraw your Account, all items are processed overnight at the end of each Business Day (which excludes Saturdays,

Sundays and federal holidays). Each Business Day, your starting available Account balance is determined in accordance with our Funds

Availability Policy. Please read the Funds Availability Policy for a detailed discussion of how and when we make funds available to you.

For (i) Checking Accounts and (ii) Money Market Accounts with check access, items are processed as follows:

a) First, deposits that have become available to you that Business Day in accordance with our Funds Availability Policy are added to your available

Account balance.

b

) Second, all withdrawals are deducted from your available Account balance in chronological date and time order based on the information

that we receive for each item. The following transaction fees will also be deducted in chronological date and time order based on when they

are assessed: wire transfer fees and overdraft fees. For some items, we do not receive date and time information. We assign these items a date

and time, which may vary from when the transactions were conducted. All checks drawn upon your Account that are not cashed at a TD Bank

Store are assigned a time of 11:00 p.m. ET on the date we receive them. If multiple items have the same date and time information, they will be

processed in the following order: (i) deposits irst; (ii) checks drawn upon your Account next, from lowest to highest check number, and then

(iii) other withdrawals, from lowest to highest dollar amount. For purposes of this section (b), withdrawals include transactions that have been

presented for payment as well as pending debit card, ATM, or electronic transactions that have been authorized but not yet presented to us for

payment. Please see the additional details below for more information regarding pending transactions.

c) Third, we add to or

deduct from your available Account balance any transactions initiated by us, such as interest credits or fees not described in

section (b) above. Examples of these fees include non-TD ATM fees, monthly maintenance fees, and paper statement fees.

4

For (i) Savings Accounts, (ii) Money Market Accounts with no check access, and (iii) CD Accounts, items are processed as follows:

a

) First, deposits that have become available to you that Business Day in accordance with our Funds Availability Policy are added to your

available Account balance.

b

) Next, the total amount of any “pending” debit card, ATM and other electronic transactions that have been authorized but not yet presented

to us for payment is deducted from your available Account balance. Please see the additional details below for more information regarding

pending transactions.

c) We then deduct items from your available Account balance by category, in the following order:

i. Outgoing wire transfers, return deposit items, and debit adjustments to your available Account balance;

ii. Overdraft fees;

iii. All other Account fees (except as described in (iv) below), and all other items including checks, ATM transactions, and debit card

transactions; and

iv. Fees assessed at the end of the statement cycle including, for example but not limited to, monthly maintenance fees.

Within categories i, ii, and iii, we post items in order from lowest to highest dollar amount.

Additional Details Regarding your Available Account Balance:

Your available Account balance is our most recent record of the amount of money available in your account for your use or withdrawal. Except as

otherwise set forth below, your available Account balance is reduced by any “pending” debit card transactions (purchases or ATM withdrawals),

and includes any deposited funds that may have been made available to you pursuant to our Funds Availability Policy.

Your available Account balance may change during the course of a day as transactions occur. The available Account balance provided to you by

the Bank may not include all of your transactions, such as checks you have written that have not yet cleared or upcoming automatic payments.

You agree that it is your responsibility to keep track of your transactions as you make them in order to avoid overdrafts and fees.

Your monthly account statement does not report pending transactions affecting your account on any given day; as a result, the daily balances

reported in your statement may not relect your available Account balance(s) occurring on that day.

Additional details regarding pending transactions for all Accounts:

When you use a debit card, ATM card, or other electronic means to make withdrawals, we may receive notice of the transaction before it is

actually presented to us for payment. That notice may be in the form of a merchant authorization request or other electronic inquiry. Upon receipt

of such notice, we treat the transaction as “pending” at the time we receive notice, and subject to certain exceptions, we deduct the amount of

the pending transactions from your available Account balance to determine the amount available to pay other items presented against your

Account. The amount of a pending transaction may not be equal to the amount of the actual transaction that is subsequently presented for

payment and posted to your Account. If a pending transaction is not presented for payment within three (3) Business Days after we receive notice

of the transaction, we will release the amount of the pending transaction. We do not deduct the amount of pending debit card transactions from

your available Account balance for certain categories of merchants that frequently request authorization for amounts in excess of the likely

transaction amount, including hotels and resorts, airlines and cruise lines, car rental companies, and automated gas pumps (pay at the pump).

Additional details regarding our processing order of items for all Accounts:

The order in which items are processed may affect the total amount of overdraft fees incurred. See “Overdrafts” below, as well as the Personal Fee

Schedule, for more information.

We may from time to time change the order in which we accept, pay, or charge items to your Account, even if (a) paying a particular item

results in an insuficient available balance in your Account to pay one or more other items that otherwise could have been paid out of your

Account; or (b) using a particular order results in the payment of fewer items or the imposition of additional overdraft fees. If we do change our

processing order for checks and other items presented for payment from your Account, we will provide advance notice of the change.

Please call 18887519000 for additional information about our processing order.

Reasons Why We May Refuse to Pay an Item:

a) is illegible;

b) is drawn in an amount greater than the amount of funds then available for withdrawal in your Account (see the Funds Availability Policy) or

w

hich would, if paid, create an overdraft;

c) b

ears a duplicate check number;

d) we believe has been altered;

e) we believe is otherwise not properly payable; or

f) we believe does not bear an authorized signature;

g) is a check drawn against a TD Essential Banking Account

We are not required to honor any restrictive legend on checks you write unless we have agreed in writing to the restriction. Examples of restrictive

legends are “Not Valid For More Than $1000”, “Void If Not Negotiated Within 30 Days of Issuance”, and the like.

Postdated Items

For Accounts with check access, you ag

ree that when you write a check, you will not date the check in the future. If you do, and the check is

presented for payment before the date of the check, we may either pay it or return it unpaid. You agree that if we pay the check, the check will be

posted to your Account on the day we pay the check. You further agree that we are not responsible for any loss to you in doing so.

P

re-authorized Drafts

If you voluntarily give information about your Account (such as our routing number and your Account number) to a party who is seeking to sell you

goods or services, and you do not physically deliver a check to the party, any debit to your Account initiated by the party to whom you gave the

information is deemed authorized by you.

5

Overdrafts

An overdraft occurs when your available Account balance is not suficient to cover a transaction, but we pay it anyway. We use your available

Account balance to determine whether you have enough money in your account to pay an item when it is presented for payment. If your

available Account balance is insuficient to pay an item when it is processed and posted in the order set forth above (see Processing Order

section), we may, in our sole discretion, pay the item (creating an overdraft) or return the item unpaid. Overdrafts may be casued by, but are

not limited to, advances to cover a check, in-person withdrawal, ATM withdrawal, debit card point-of sale transaction, withdrawal by other

electronic means from your Account, or preauthorized payments. A preauthorized payment may include automatic bill payments, Online and

Mobile Banking transfers and payments made through Bill Pay, recurring debit card transactions, telephone transfers, Store payments, transfers

and withdrawals, or external transfers to other institutions and payments to other people.

We may charge you an overdraft fee if we pay an item that exceeds your available Account balance. The dollar amount of our overdraft fees is

set forth in our Personal Fee Schedule. If you overdraw your account, you must immediately pay all fees, overdrafts and other amounts you owe

us. These amounts may be paid out of any subsequent deposit to your account.

We will not charge more than three (3) overdraft fees per account per any one Business Day. You will not be charged overdraft fees for ATM or

one-time debit card transactions unless you have enrolled in TD Debit Card Advance (see “Important Information for Consumers about your TD

Bank Checking Account” brochure for more information).

For TD Essential Banking Accounts: We may decline or return items that exceed your available Account balance. Some items, including

preauthorized payments, may post to your account even though they overdraw your available Account balance; we will not assess your TD

Essential Banking Account an overdraft fee in those instances.

For (i) Savings Accounts and (ii) Money Market Accounts with no check access: You may be charged an overdraft fee(s) on any item(s)

presented for payment regardless of your available Account balance at the end of the day. Please be aware that merchants and other third

parties sometimes re-submit items that we return unpaid. Each re-submission constitutes a separate item. You agree that if any transaction is

submitted for payment again after having previously been returned unpaid by us, an overdraft fee may be assessed each time the transaction is

submitted for payment and your available balance is insuficient to pay the item.

For (i) Checking Accounts and (ii) Money Market Accounts with check access: You will not be charged an overdraft fee for items that overdraw

your available Account balance by our Overdraft threshold of $50 or less when presented for payment (see Processing Order section).

Pending debit card transactions reduce your available Account balance to pay other items (see Processing Order section). If other items are

presented for payment that exceed the available Account balance (as reduced by the pending transaction(s)), you may incur an overdraft fee.

Please read our Funds Availability Policy for a detailed discussion of how and when we make funds available to you. If you withdraw funds before

they become available, you may incur an overdraft fee.

You agree to pay us, when we ask you, all of our costs of collecting an overdraft, to the fullest extent permitted by applicable law. These costs

include, but are not limited to, our legal fees and expenses. If more than one of you owns an Account, each of you will be responsible for paying us

the entire amount of all overdrafts and obligations resulting from the overdrafts.

The Bank is not obligated to pay any item that exceeds your available Account balance and may cease paying overdrafts at any time without

prior notice of reason or cause. It may be a crime to intentionally withdraw funds from an Account when there are not enough funds in the

Account to cover the withdrawal or when the funds are not yet available for withdrawal.

Overdraft Grace: Eligible Checking Accounts and Money Market Accounts with check access include Overdraft Grace. Overdraft Grace affords

you additional time to bring your available Account balance to $0 or greater than $0 following an overdraft to receive an automatic refund of

applicable overdraft fee(s).

Subject to the below, with Overdraft Grace, if you overdraw your Account by more than $50 but make suficient deposits to bring your available

Account balance back to $0 or greater than $0 as of 11:00 p.m. ET on the next Business Day following the day on which the item(s) that overdrew

your Account posted to your Account (the “Overdraft Grace Period”), we will refund the overdraft fee(s) that were assessed to your Account for

those item(s). For example, if an item was presented to us for payment on Monday, and it overdrew your available Account balance, you will

have until 11:00 p.m. ET on the next Business Day (Tuesday) to bring your available Account balance back to $0 or greater than $0 to receive an

automatic refund of overdraft fees assessed for this item. All deposits are subject to our Funds Availability Policy.

Depending on the type of deposit(s) and/or the time of deposit(s), some or all of your deposit(s) may not be available before the Overdraft Grace

Period expires. For example, if you make a $500 check deposit and only $100 becomes available within the Overdraft Grace Period, that deposit

may not be suficient to bring your available Account balance back to $0 or greater than $0 within the Overdraft Grace Period. For additional

information on when funds become available, please refer to the Processing Order and Funds Availability Policy sections of this Agreement.

With Overdraft Grace, if you do not make suficient deposits to bring your available Account balance back to $0 or greater than $0 within the

Overdraft Grace Period, then we will not refund overdraft fee(s) for those item(s).

If you further reduce your available Account balance during the Overdraft Grace Period through additional debits from your Account (including

pending debit card transactions), this will increase the deposit amount needed to bring your available Account balance to $0 or greater than $0

within the Overdraft Grace Period to receive an overdraft fee refund. For example, if you overdraw your account by $100 on Monday and make a

deposit of $150 on Tuesday to bring your available Account balance greater than $0, but on Tuesday, you make a $100 debit card transaction,

you will need to deposit an additional $50 as of 11:00 p.m. ET on Tuesday to receive an overdraft fee refund for the item(s) that overdrew your

Account on Monday.

If a deposit is received and later returned, we may assess or reassess an overdraft fee that was refunded. By way of example, we may provide

provisional or inal credit for an item that is deposited or credited to your Account and later returned or debited from your Account pursuant to an

adjustment, levy, returned item, court order, court proceedings, seizure warrant, request from law enforcement or request from another inancial

institution may not prevent the assessment of an overdraft fee. Such an item, notwithstanding the provisional or inal credit, may not be an

eligible deposit.

While Overdraft Grace affords you additional time to receive automatic refunds for overdraft fees, it does not prevent other actions on your

Account, including but not limited to Account closure. Additionally, Overdraft Grace will not prevent reporting to regulatory or administrative

agencies that may be required by federal, state or other law for certain types of accounts, including but not limited to real estate escrow and

attorney trust accounts.

O

verdraft Grace may not be available for accounts in a suspended or frozen status or on hold, or accounts that are subject to court proceedings,

court order, seizure warrant, forfeiture, restraining notice, levy, garnishment or a request from law enforcement, state or federal agencies or other

inancial institutions.

6

Stop Payments

At your request and risk, the Bank will accept a stop payment request for a check on your Account for a fee (see Personal Fee Schedule). To be

effective, a stop payment request must be received in such timely manner so as to give the Bank a reasonable opportunity to act on it, and must

precisely identify the Account number, check number, date and amount of the item, and the payee.

Yo

ur stop payment request will be effective after the request has been received by the Bank and the Bank has had a reasonable opportunity to

act on it. Regardless of whether your stop payment request has been made orally or in writing, it will remain in effect for one (1) year from the date

i

t was given. If your stop payment request has been made orally, the Bank will send you a written conirmation. If your stop payment request is

made in writing, you must use a form that is supplied by the Bank; this form will constitute written conirmation of your request. In either case, it

is your responsibility to ensure that all of the information supplied on your written conirmation is correct and to promptly inform the Bank of any

inaccuracies.

To maintain the validity of the stop payment request for more than one (1) year, you must furnish a new stop payment request that is conirmed in

writing as described in the preceding paragraph before the expiration of the one (1) year period. If a new stop payment request is not received, the

check may be paid.

We are not liable for failing to stop payment if you have not given us suficient information or if your stop payment request comes too late for us

to act on it. We are entitled to a reasonable period of time after we receive your stop payment request to notify our employees and take other

action needed to stop payment. You agree that “reasonable time” depends on the circumstances, but that we will have acted within a reasonable

time if we make your stop payment request effective by the end of the next Business Day following the Business Day on which we receive your

stop payment request. If we stop payment, you agree to defend and pay any claims raised against us as a result of our refusal to pay the check or

other item on which you stopped payment.

If we recredit your Account after we have paid a check or other item over a valid and timely stop order, you agree to sign a statement describing

the dispute you have with the person to whom the check or item was made payable. You also agree to transfer to us all of your rights against the

payee and any other holder, endorser or prior transferee of the check or item and to cooperate with us in any legal action taken to collect against

the other person(s).

If we are liable for inadvertently paying your check over a stop payment order, you must establish the amount of your loss caused by our payment

of the check. We will pay you only the amount of the loss, up to the face amount of the check. You agree that we shall not be liable for any

punitive, exemplary or consequential damages.

The Bank has no duty to stop payment on a cashier’s check, teller’s check, or other similar item because items of this type are not drawn on your

Account. The Bank may, in its sole discretion, attempt to stop payment on a cashier’s check, teller’s check or other similar item if you certify to

our satisfaction that the item has been lost, stolen or destroyed. You must also furnish any other documents or information we may require, which

may include your afidavit attesting to the facts and your indemniication of the Bank. Even if the Bank agrees to attempt to stop payment on a

cashier’s check, teller’s check or other similar item, if the item is presented for payment, the Bank may pay it and you will be liable to us for that

item, unless otherwise required by applicable law.

For information on Stop Payments as they pertain to pre-authorized funds transfers, please reference the Pre-authorized (Recurring) Transfers and

Stop Payments section within Part IV: Electronic Funds Transfers Disclosure.

International, ACH, The Clearing House Real-Time Payments (“TCH RTP”) and Wire Transactions

If your Account receives incoming ACH transactions (either credits or debits), RTP transfers, or wire transfers initiated from within or outside of

the United States, both you and we are subject to the Operating Rules and Guidelines of the National Automated Clearing House Association

(“NACHA”), the The Clearing House Real-Time Payments (TCH RTP) Operating Rules,” or the rules of any wire transfer system involved, and the laws

enforced by the Ofice of Foreign Assets Control (“OFAC”). You must not send or receive RTP transfers on behalf of a person who is not a resident

of, or otherwise domiciled in, the United States. Under such rules and laws, we may temporarily suspend processing of a transaction for greater

scrutiny or veriication against the OFAC list of blocked parties, which may result in delayed settlement, posting, and/or availability of funds. If we

determine there is a violation, or if we cannot satisfactorily resolve a suspected or potential violation, the subject funds will be blocked as required

by law. If you believe you have adequate grounds to seek the return of any blocked funds, it is your sole responsibility to pursue the matter with

the appropriate governmental authorities. Please see the OFAC website for procedures and form required to seek a release of blocked funds.

We may impose a fee, as disclosed on the Personal Fee Schedule, for any domestic or international incoming wire transactions. Wire transfers in a

foreign currency will be converted at our rate of exchange on the day the transaction completed and we may earn revenue on this exchange.

Periodic Statements; Time Limit to Report Errors

If your Account is not a Holiday Club, Club Saver, IRA, Passbook, or CD Account, the Bank will provide you with a periodic statement. Unless you

tell us of a change of address, we will continue to mail or deliver electronically statements or any other notices to your address as it appears on

our records and you will be considered to have received those statements and any other notices sent to you at that address. We do not have to

send you a statement or notice if (i) you do not claim your statement, (ii) we cannot deliver your statement or notice because of your instructions

or your failure to tell us that you have changed your address, or (iii) we determine that your Checking Account has been inactive for more than 6

months or your Savings Account has been inactive for more than 9 months.

You should review your statements and balance your Account promptly after you receive them or, if we are holding them for you, promptly after

we make them available to you. If you don’t receive an Account statement by the date when you usually receive it, call us at once. You must

review your statements to make sure that there are no errors in the Account information.

On Accounts with check-writing privileges, you must review your statement and imaged copies of paid checks, if any, we send you and report

forgeries, alterations, missing signatures, amounts differing from your records, or other information that might lead you to conclude that the

check was forged or that, when we paid the check, the proper amount was not paid to the proper person. You have this duty even if we do not

return checks to you or we return only an image of the check. You should notify us as soon as possible if you think there is a problem.

Applicable law and this Agreement require you to discover and report any error in payment of a check within speciied time periods. You agree

that statements and any images of paid checks accompanying the statement shall be deemed to be “available” to you as of the statement

mailing date, or the date on which electronic statements are available for viewing. If we are holding your Account statements for you at your

request, the statements become “available” on the day they are available for you to pick up. This means, for example, that the period in which you

must report any problem with an Account begins on the day we make the statement available, even if you do not pick up the statement until later.

7

If you assert against us a claim that an item was not properly payable because, for example, the item was forged or an endorsement was forged,

you must cooperate with us and assist us in seeking criminal and civil penalties against the person responsible. You agree to assist TD Bank, N.A.

and law enforcement authorities as needed in any investigation and, if needed, to serve as a witness at any hearing, proceeding or action brought

against the person(s) responsible for the forgery. If we ask, you also must give us a statement, under oath, about the facts and circumstances

relating to your claim. If you fail or refuse to do these things, we will consider that you have ratiied the defect in the item and agree that we may

charge the full amount of the item to your Account.

Yo

u must notify us as soon as possible if you believe there is an error, forgery or other problem with the information shown on your Account

statement. You agree that thirty (30) Calendar Days after we mailed a statement (or otherwise made it available to you) is a reasonable

amount of time for you to review your Account statement and report any errors, forgeries or other problems. In addition, you agree not to

assert a claim against us concerning any error, forgery or other problem relating to a matter shown on an Account statement unless you

notiied us of the error, forgery or other problem within thirty (30) Calendar Days after we mailed you the statement (or otherwise made it

available to you). This means, for example, that you cannot bring a lawsuit against us, even if we are at fault, for paying checks bearing a

forgery of your signature unless you reported the forgery within thirty (30) Calendar Days after we mailed you the statement (or otherwise

made it available to you) listing the check we paid. If the same person has made two or more unauthorized transactions and you fail to notify

us of the irst one within this 30-day period, we won’t be responsible for unauthorized transactions made by the same wrongdoer.

There are exceptions to this 30 day notice requirement. For claims asserting forged, missing or unauthorized endorsement or alteration, you must

notify us within the period speciied by the state law applicable to your Account. We may destroy original checks not less than thirty (30) Calendar

Days after the statement mailing date or electronic delivery date. We will retain copies of the front and back of the checks on microilm or other

media for a period of seven (7) years. During that period, we will provide you an imaged copy of any paid check on request, but we need not do so

thereafter. You agree not to make any claim against us arising out of the authorized destruction of your original checks or the clarity or legibility of

any copy we provide.

Combined Statements with Checking

I

f more than one Checking type Account is combined together on a monthly statement, then only one Checking Account can be designated as

the primary Account. This primary Account may receive imaged copies of the paid checks back with the statement, and we may impose a fee as

disclosed on the Personal Fee Schedule, for providing these imaged copies. Checks for all other Accounts will be retained by the Bank. To request

a copy of a paid check, please call 18887519000.

Please note that a Health Savings Account cannot be included on a combined statement.

Important Information for Opening a New Account

To help the government ight the funding of terrorism and money laundering activities, Federal law requires all inancial institutions to obtain,

verify and record information that identiies each person who opens an Account. When you open an Account, we will ask for your name, legal

address, date of birth, Social Security or Tax Identiication Number, and other information that will allow us to identify you. We may also ask to see

your driver’s license or any other identifying documents.

Te

lephone Numbers

If you give a cell phone number directly to us, you consent to and agree to accept calls and text messages related to the servicing of your

Account to your cell phone from us and our agents. For any service related telephone calls, cell phone calls, or text messages placed to you

by us or our agents, you consent and agree that those calls may be automatically dialed and/or may consist of pre-recorded messages.

Text message & data rates may apply. User can reply HELP for help with text messages or STOP to stop text messages.

Ac

count Ownership

The following provisions explain the rules applicable to your Account depending on the form of ownership speciied on the signature card.

Only the portion corresponding to the form of ownership speciied will apply.

Individual Accounts

An individual Account is issued to one person who does not intend (merely by opening the Account) to create any survivorship rights for any

other person.

Jo

int Accounts – With Right of Survivorship

A joint Account is issued in the name of two or more persons. If more than one of you opens an Account and signs a signature card as a co-owner

of the Account, the Account is a joint Account with right of survivorship. Each of you intends that, upon your death, the balance in the Account

(subject to any previous pledge to which we have consented) will belong to the survivor(s), and we may continue to honor checks or orders drawn

by, or withdrawal requests from, the survivor(s) after the death of any owner(s). If two or more of you survive, you will own the balance in the

Account as joint tenants with right

of survivorship.

If you are under the age of 18, you

must open a joint Account with a parent or legal guardian as the secondary owner.

T

he following rules apply to all joint Accounts:

a

) Deposits: All deposits are the property of all of the owners of the Account. Each owner of a joint Account agrees that we may credit to the joint

Account any check or other item which is payable to the order of any oe or more of you, even if the check or other item is endorsed by less

than all or none of you. We may supply endorsements as allowed by law on checks or other items that you deposit to the Account. For certain

checks, such as those payable by the government, we may require all payees to endorse the check for deposit.

b

) Orders: The Bank may release all or any part of the balance of the Account to honor checks, withdrawals, orders, or requests signed by any

owner of the Account. Any one of you may close the Account. We may be required by service of legal process to hold or remit funds held in a

joint Account to satisfy an attachment or judgment entered against, or other valid debt incurred by, any owner of the Account. None of you may

instruct us to take away any of the rights of another. If there is a dispute among you, you must resolve it yourselves and the Bank does not have to

recognize that dispute in the absence of any valid court order. Unless we receive written notice signed by any owner not to pay any joint deposit,

we shall not be liable to any owner for continuing to honor checks or other orders drawn by, or withdrawal requests from, any owner; after receipt

of any such written notice, we shall not be liable to any owner for refusing to pay any checks or honor any orders and we may require the written

authorization of any or all owners for any further payments.

c) L

iability: Co-owners of a joint Account are jointly and severally liable for activity on this Account. In the event of any overdrafts on a joint

Account, the joint owners agree that each owner shall be jointly and severally liable for the overdrafts in the joint Account, whether or not any

particular owner: (a) created the overdraft, (b) had knowledge of the overdraft, (c) was involved in or participated in activity in the Account, or

(d) derived any beneit from the overdraft.

8

No Two-Signer Accounts

We do not offer Accounts on which two or more signatures are required for a check or other withdrawal. Notwithstanding any provisions to the

contrary on any signature card or other agreement you have with us, you agree that if any Account purports to require two or more signers on

items drawn on or withdrawals from the Account, such provision is solely for your internal control purposes and is not binding on us. If more than

one person is authorized to write checks or draw items on your Account, you agree that we can honor checks signed by any Authorized Signer,

even if there are two or more lines on the items for your signature and two signatures are required.

Specialty Accounts

TD Bank offers Accounts providing beneits to speciic demographics. The following provisions explain the rules to these specialty Accounts.

a) TD Complete Checking:

i. TD Complete Checking for young adults: TD Complete Checking accounts provide a monthly maintenance fee waiver and free non-TD ATM

fee for primary account owners age 17 through 23. The monthly maintenance fee waiver expires upon the primary Account owner’s 24th

birthday at which time the Account will be subject to the monthly maintenance fee unless the following are met: Maintain a $500 minimum

daily balance or maintain $500 Direct Deposits per statement period or have $5,000 relationship balance across linked TD deposit accounts.

ii

. TD Complete Checking for adults aged 60 and above: TD Complete Checking accounts provide free paper statements and standard checks

for primary account holders aged 60 and above:

b) TD Essential Banking: TD Essential Banking

will not charge any overdraft fees; however, you will not have the ability to order TD checks and

there are no check writing privileges.

TD Essential Banking Accounts provide a monthly maintenance fee waiver for primary Account owners age 13 through 17. The monthly

maintenance fee waiver expires upon the primary Account holder’s 18th birthday at which time the Account will be subject to the monthly

maintenance fee.

Trust Accounts

a) Unwritten: If your Account is designated as a trust Account, in the absence of any written trust agreement provided to us at Account opening,

this Account is deemed a Revocable Unwritten Trust, and you as trustee may withdraw all of the funds during your lifetime. In the event of your

death, the Account will belong to the person you named as Account beneiciary, if that person is still living. That Account beneiciary would

have the sole right to withdraw the funds in the Account at anytime after your death (although the Bank may be entitled under applicable law

to place a hold on the funds before payment to the beneiciary), but not before.

b) Written: If you have opened the Account as trustee of a written trust or as trustee pursuant to court order, only the trustee will be allowed to

withdraw funds or otherwise transact business on the Account as designated by the trust instrument or court order. We can request a certiied

copy of any trust instrument or court order, but whether or not a copy is iled with us, we will not be held responsible or liable to any of the

written trust’s beneiciaries for the trustee’s actions. Beneiciaries acquire the right to withdraw only as provided in the trust instrument or

court order.

The person(s) creating either of these Trust Account types may make changes to the Account, including changes to the beneiciaries or the

Account type, and may withdraw funds on deposit in the Account, only as permitted by the trust instrument or court order.

Some jurisdictions have speciic laws governing other speciic types of iduciary Accounts. If you establish one of these types of Accounts, you

agree to comply with all of the laws applicable to such types of Accounts.

With all iduciary and custody Accounts, regardless of whether a written trust instrument has been provided to us, the owners and beneiciaries

of the Account agree that we will not be liable if the trustee or custodian commits a breach of trust or breach of iduciary duty, or fails to comply

with the terms of a written trust agreement or comply with applicable law. We are not responsible for enforcing the terms of any written trust

agreement or applicable law against the trustee or custodian, and can rely on the genuineness of any document delivered to us, and the

truthfulness of any statement made to us, by a trustee or custodian.

Uniform Gifts/Transfers To Minors Act Account

If your Account is opened under the Uniform Transfers to Minors Act or Uniform Gifts to Minors Act, the funds in the Account belong to the minor

[depending on the jurisdiction in which you have opened such an Account and the circumstances, a minor may be a child under the age of

eighteen (18) or under the age of twenty-one (21)] you have named. You must provide to us the minor’s Social Security Number. You, as custodian,

or the custodian you have named, may withdraw all of the funds in the Account at any time for the beneit of the minor you have named. Our

contractual obligation to honor checks, orders, withdrawals or other requests related to the Account is with the custodian only. In the event of the

custodian’s death, the person named as successor custodian (as provided by law) will succeed to these rights. When the minor reaches the age of

majority applicable in his or her jurisdiction, or at another time determined by applicable law, the custodian shall transfer any funds remaining in

the Account to the minor or to the minor’s estate.

Power of Attorney

We may, in our sole discretion (unless we are required by law to recognize a statutory form of power of attorney), recognize the authority of a

person to whom you have given a power of attorney to enter into transactions relating to your Account, until and unless we receive written notice

or we have actual notice of the revocation of such power of attorney. However, you must show us an original copy or certiied copy of the power

of attorney, properly notarized, and any other documentation we may ask for from time to time. The power of attorney and all other documents

must be in a form satisfactory to the Bank. We will not be liable for damages or penalty by reason of any payment made to, or at the direction of, a

person holding a power of attorney.

Certiied Taxpayer Identiication Number (“TIN”) or Social Security Number (“SSN”)

Federal law requires you to provide to the Bank a valid and certiied Taxpayer Identiication Number (“TIN”) or Social Security Number (“SSN”). We

may be required by federal or state law to withhold a portion of the interest credited to your Account in the following circumstances:

a) you do not give us a correct TIN or SSN;

b) the IRS tells us that you gave us an incorrect TIN or SSN;

c) the IRS tells you that you are subject to backup withholding because you have under-reported your interest or other income;

d) you fail to certify to us that you are not subject to backup withholding;

e) you do not certify your TIN or SSN to us; or

f) there may be other reasons why we may be required to do so under applicable law.

If we do this, the amount we withhold will be reported to you and the IRS and applied by the IRS to the payment of any Federal income tax you

may owe for that year.

9

Credit Veriication and Obtaining Financial Information

You agree that we may verify credit and employment history through third parties, including but not limited to consumer reporting agencies,

or verify any previous banking relationships of yours for any Accounts you

have with the Bank now or in the future. If an Account is declined based on adverse information, you may request from the consumer reporting

agency a copy of the information supplied to us. Additionally, if your Account is closed for insuficient funds activity or other negative reason,

a report may be made by us to one or more consumer reporting agencies or other third parties if permitted by applicable law. Please notify us

if you have a dispute or if you have questions regarding the information we provide. Write to us at: TD Bank, Mailstop ME02002036, P.O. Box

9547, Portland, ME 04112. Please provide your name, Account number, and why you believe there is an inaccuracy or describe the item you are

not sure about. We will complete any investigation and notify you of our indings and, if necessary, corrections. Please note that calling us will not

preserve your rights. If you are a licensed attorney, you agree that we may report information about overdrafts on and/or returned checks drawn

on Accounts which you maintain as trustee for the beneit of another person or in any iduciary capacity, to the extent and in the manner required

by applicable laws, rules, or regulations. You agree that we have no liability to you for reporting any information to applicable authorities regarding

any Account which we believe in good faith is subject to such laws, rules, or regulations. If you’re having trouble with payments, lenders want to

explore options with you. Visit td.com or reach out to the National Foundation for Credit Counseling online or by phone at 18773576322 for help.

Conlicting Demands/Disputes

If there is any uncertainty or conlicting demand regarding the ownership of an Account or its funds; or we are unable to determine any person’s

authority to give us instructions; or we are requested by law enforcement or a state or local agency to freeze the Account or reject a transaction

due to the suspected inancial abuse of an elder or dependent adult; or we believe a transaction may be fraudulent or may violate any law, we

may, in our sole discretion:

1) freeze the Account and refuse transactions until we receive written proof (in form and substance satisfactory to us) of each person’s right and

authority over the Account and its funds;

2) close the Account and distribute the Account balance, subject to any debts or obligations owed to the Bank, equally to each Accountholder, or

close the Account and distribute funds to a victim of a fraudulent scheme or the rightful owner of the funds, which may be determined by us in

our sole discretion;

3) refuse transactions and return checks, marked “Refer to Maker” (or similar language);

4) require the signatures of all authorized signers for the withdrawal of funds, the closing of an Account, or any change in the Account regardless

of the number of authorized signers on the Account;

5) request instructions from a court of competent jurisdiction at your expense regarding the Account or transaction; and/or

6) continue to honor checks and other instructions given to us by persons who appear as authorized signers according to our records. The

existence of the rights set forth above shall not impose an obligation on us to assert such rights or to deny a transaction.

If any person notiies us of a dispute, we do not have to decide if the dispute has merit before we take further action. We may take these actions

without any liability and without advance notice, unless the law says otherwise

Changing Your Account

If we agree to let you make any change to your Account type in the middle of the Account’s interest and/or service charge cycle, without requiring

you to open a new Account and without changing your Account number, you agree that the following rules will apply to the period in which we

allow you to make this change:

a) Interest: The rules for the payment of interest (if any) on the new Account will take effect on the day the type of Account is changed (the