Produced by:

RKG Associates Inc. for MSHDA

March 2019

CONTENTS

ACKNOWLEDGEMENTS .................................................................................................................................................... 5

EXECUTIVE SUMMARY ...................................................................................................................................................... 9

Project Purpose ............................................................................................................................................................... 9

Key Themes .................................................................................................................................................................... 9

Key Findings ................................................................................................................................................................. 10

Recommendations to Advance Homeownership .................................................................................................... 11

INTRODUCTION ................................................................................................................................................................ 12

Project Purpose ............................................................................................................................................................. 12

Defining Affordability ................................................................................................................................................. 15

OVERARCHING THEMES ................................................................................................................................................ 16

Population, Wages and Purchasing Power .............................................................................................................. 16

Housing Inventory ....................................................................................................................................................... 19

Development Costs ...................................................................................................................................................... 22

Barriers to Homeownership ....................................................................................................................................... 24

CASE STUDIES .................................................................................................................................................................... 26

Urban Affordability – Grand Rapids ......................................................................................................................... 26

Urban with Economic Challenges - Saginaw ........................................................................................................... 33

Aging Suburb - Westland ........................................................................................................................................... 40

Small Town Rural - Alpena ........................................................................................................................................ 46

STRATEGIES TO ADVANCE HOMEOWNERSHIP OPPORTUNITIES ..................................................................... 52

Finance Tools ................................................................................................................................................................ 54

Rehabilitation and Preservation Tools ...................................................................................................................... 58

Land Use and Zoning Tools ....................................................................................................................................... 62

Economic Development Tools .................................................................................................................................... 65

DATA SOURCES AND METHODOLOGY...................................................................................................................... 69

ACKNOWLEDGEMENTS

Michigan State Housing Development Authority

Laurie Cummings, Project Manager

Gary Heidel, Acting Executive Director

Mary Townley, Director, Homeownership

David Allen, Manager, Office of Market Research

Michigan Homeownership Study Advisory Committee

Katharine Czarnecki, Michigan Economic Development Corporation

Shanna Draheim, Michigan Municipal League

Kathie Feldpausch, Michigan Realtors

Luke Forrest, Michigan Municipal League

Patricia Herndon, Michigan Bankers Association

Larry Merrill, Michigan Townships Association

Sandra Pearson, Habitat for Humanity of Michigan

Jamie Schriner, formerly of The Community and Economic Development Association of Michigan

Lee Schwartz, Michigan Homebuilders Association

Michael Selden, Michigan Townships Association

Charlotte Smith, Local Initiative Support Corporation

Troy Villanueva, The Community and Economic Development Association of Michigan

Special Thanks To:

The Michigan Realtors, particularly Kathie Feldpausch, who helped the research team connect with

the leaders of each regional MLS in Michigan to obtain sales data that was integral to this study. We

would also like to thank each of the MLS region leaders across the state of Michigan who provided

current and historic sales data to the team.

The staff in Grand Rapids, Saginaw, Westland, and Alpena who provided us with a wealth of

information on their communities and helped highlight specific housing and economic challenges for

our case studies.

Each of the 80+ interviewees that took time to speak with us and discuss the challenges and

opportunities facing the communities, businesses, and people of the State of Michigan.

FOR ADDITIONAL INFORMATION, PLEASE CONTACT:

Laurie Cummings, Michigan State Housing Development Authority

CummingsL@michigan.gov, (517)-373-6744

735 E. Michigan Avenue, Lansing, Michigan 48909

A MESSAGE FROM THE ADVISORY COMMITTEE

Dear Reader,

The supply of affordable homes for sale in Michigan is not meeting demand, and the share of

Michigan citizens who own a home is falling as a result. The Michigan State Housing

Development Authority (MSHDA) commissioned the Michigan Homeownership Study to

investigate the scope and causes of the problem and suggest some ways to address it.

As members of the Advisory Committee for this effort, we are pleased to have helped create the

first-ever statewide affordable homeownership study of this type in Michigan. The Advisory

Committee provided guidance and input into the study and helped researchers access data and

information that could not have been accessed otherwise.

While the Michigan Homeownership Study Advisory Committee represents highly diverse interests

in the homeownership arena, all of us have a stake in finding solutions to the state’s lack of

affordable for-sale homes. Homeownership strengthens communities, enables families to build

equity, and makes important contributions to the economy. It is the sincere wish of the Advisory

Committee members that the information in this document will result in action from

policymakers, local governments, nonprofits, and others in the housing industry. This problem

will not go away on its own.

Sincerely,

Shanna Draheim, Michigan Municipal League

Luke Forrest, Michigan Municipal League

Kathie Feldpausch, Michigan Realtors®

Patricia Herndon, Michigan Bankers Association

Larry Merrill, Michigan Townships Association

Katharine Czarnecki, Michigan Economic Development Corporation

Sandra Pearson, Habitat for Humanity of Michigan

Jamie Schriner, formerly of The Community and Economic Development Association of Michigan

Lee Schwartz, Michigan Homebuilders Association

Michael Selden, Michigan Townships Association

Charlotte Smith, Local Initiative Support Corporation

Troy Villanueva, The Community and Economic Development Association of Michigan

MICHIGAN HOMEOWNERSHIP STUDY 9

EXECUTIVE SUMMARY

Project Purpose

Home prices across parts of Michigan have risen significantly over the last decade, and generally,

supply has not kept pace with demand. Housing affordability and price security are critical

components for creating places where residents can live comfortably without feeling stretched

financially. As housing prices rise alongside most other monthly expenses, more and more households

are having a tough time adjusting to the rising cost of living. The goal of the Michigan

Homeownership Study is to analyze and identify the needs and gaps in the homeownership market

across Michigan.

This report is organized in two complementary pieces: the Michigan Homeownership Study and its

companion document the Michigan Homeownership Study: Key Trends and Measures by Prosperity

Region. Used in tandem, these reports present a multi-level analysis that can help inform policy-

makers at the state, regional, and local levels about the historical, current, and future challenges in the

for-sale housing market. The companion document is a compilation of state and regional analyses

relating to demographics, socioeconomics, and the for-sale housing market. The Michigan

Homeownership Study document utilizes knowledge gained from the companion document and

investigates case study communities, categorizes challenges thematically, and provides

recommendations to advance homeownership opportunities.

Key Themes

Homeownership continues to be a goal of many Michigan residents, but the pathways of achieving

this goal are becoming more difficult. Michigan’s population is projected to increase, meaning new

homes will need to be built in hot markets and rehabilitation of older homes will need to be financed

to support the aggregate growth in households across the state. The cost of building or renovating

housing is a major driver of price increases as material costs, land values, and permitting times have

increased in many locations, making it more challenging for builders to offer an affordable product to

potential buyers.

Statewide sales prices for single-family homes rose by 71 percent between 2012 and 2017 with the

median sales price of a single-family home being $156,560. This is significantly less than the median

sales prices of a newly built home which is $307,970. Similarly, the statewide condominium market

experienced price increases of 73 percent over the last six years. In 2017, the median sales price of a

condominium statewide was $161,710 while the median sale price of a new condominium was

$276,550. That is a 71 percent price differential between existing and new units. The upward pricing

trend is one of the most significant barriers to entry for households across the state.

In addition to housing prices outpacing wage growth in some parts of the state, homebuyers are also

challenged by increasing levels of personal debt, diminished savings, and stricter lending

requirements by financial institutions due to the housing crisis. Purchasing power constraints limit

the ability of households to buy new homes or undertake major renovations to existing homes.

Younger householders who carry large student loan debt coupled with rapid price escalations in

MICHIGAN HOMEOWNERSHIP STUDY 10

housing markets located in urban job centers make homeownership difficult to attain and result in

greater numbers of renter households.

Michigan has a wide variety of community types each with their own challenges when it comes to

furthering homeownership opportunities. Growing urban communities face challenges of rising home

values and displacement while economically-challenged urban communities are dealing with

population decline and vacancy issues. Prospering suburbs are facing new growth pressures and

struggling with how best to repurpose land to meet today’s housing demands. Rural communities

struggle to retain younger residents to fill jobs and purchase homes, yet some see increases in seasonal

population and a loss of year-round housing stock to the second home market.

Key Findings

The following are some key findings from the homeownership study:

• Michigan’s ownership housing stock is older, and units may not have the layout, systems, or

amenities today’s homebuyers are looking for.

• Many vacant ownership units have not been maintained over time and will require substantial

rehabilitation.

• Communities with housing capacity may have declining population and fewer economic

opportunities that will attract new residents.

• Communities with housing demand as well as supply shortages are seeing prices escalate creating

an affordability issue for existing residents and those looking to locate there.

• Zoning and other regulatory barriers hold back or prolong the development process resulting in

fewer units created and higher price points.

• New employment opportunities or expansions may not be aligned with housing production or

rehabilitation to meet the demand from new employees.

• The combination of stricter lending practices due to the financial crisis of the early 2000’s, growing

debt loads from student loans and other borrowing, and wages not keeping pace with costs are

making it more difficult to purchase a home.

• Financial resources for housing programs are shrinking, forcing all levels of government to do

more with less.

MICHIGAN HOMEOWNERSHIP STUDY 11

Recommendations to Advance Homeownership

To address some of the identified issues related to homeownership, recommendations were crafted

based on the findings from the state, regional, and case study analysis. Recommendations are grouped

under four categories, each addressing a larger-scale issue impacting homeownership in Michigan.

• Finance Tools. Access to capital, whether for an individual buyer or a developer, is critical to

ensuring home construction and home purchases. Whether providing down payment

assistance for a first time homebuyers, or incentives to developers, different markets require

different finance tools. Recommendations found under this category offer ways to address

financing gaps and bolster existing programs.

• Rehabilitation & Preservation Tools. Across some parts of Michigan, communities and

regions are facing high vacancy rates, deferred maintenance, and homes that are not ready to

re-enter the market. Buyers in weaker market areas are finding it difficult to pull together

financing to both purchase a home and complete the necessary rehab due to lending criteria

and the difficulty of finding sales comps in the area. Oftentimes, the cost to rehab a unit may

be higher than the actual purchase price. Recommendations found in under this category

relate to rehabilitation funding and neighborhood stabilization/preservation tools.

• Land Use & Zoning Tools. Land use, zoning, and permitting are local tools that communities

have direct control over and impact the type of homeownership units that can be built, the

location of those units, and the time it takes to build them. Changes in regulations can help

with predictability of approvals, speed up delivery of units, and lower developer risk.

• Economic Development Tools. Housing and jobs are inextricably linked and aligning

employment opportunities with affordable housing is an important step to attracting and

retaining employees. The recommendations provide opportunities for the public sector and

private sector to act in unison to help businesses thrive and employees find housing they can

afford.

MICHIGAN HOMEOWNERSHIP STUDY 12

INTRODUCTION

Across Michigan, and nationally, home prices have risen significantly over the last decade. The

recovery from the Great Recession coupled with a low-interest rate environment has led to a general

uptick in homebuying. In many markets supply has not kept pace with demand, which is only

expected to increase over time. Circumstances have occurred in which home values have risen faster

rate than wages in many communities, leaving families and individuals priced out of the for-sale

marketplace.

Housing affordability and price security are critical components for creating places where residents

can live comfortably without feeling stretched financially. As housing prices rise alongside most other

monthly expenses, more and more households are having a tough time adjusting to the rising cost of

living. This creates a situation where households become cost burdened and are forced to spend more

than the recommended 30 percent of their monthly income on housing-related costs. For many

households, this can create a ripple effect where other monthly expenses are scaled back or cut out

completely. Food, healthcare and wellness, transportation, and child care are some of the basic

household needs that can go unmet in the face of rising housing costs.

Understanding the economic landscape both in the marketplace and across demographic groups can

help policymakers identify needs and align and direct the requisite resources towards priority areas.

Across Michigan, economic opportunity varies as do incomes; rural and urban communities may have

different needs, but a central commonality is that housing is a fundamental need which also defines a

community – a collection of households living area. Ensuring that housing is available and affordable

to all income levels is critical for growing and sustaining communities across the state.

This study, which was commissioned by MSHDA, provides information on homeownership

challenges statewide and by Michigan Prosperity Region. MSHDA has also provided directly a more

geographically detailed examination of Michigan Housing Markets through its ‘Statewide Housing

Needs Assessment.’ This data/mapping tool, which contains measures of local housing affordability

for 380+ specific housing markets in Michigan, will be available on the MSHDA web site in coming

months found at https://www.michigan.gov/mshda.

The Michigan Homeownership Study provides

context for this data tool, and can help the reader understand the larger issues that help drive the

small-area data and maps.

Project Purpose

Home prices across parts of Michigan have risen significantly over the last decade, and generally,

supply has not kept pace with demand. Additionally, new construction has trended toward rental

units at the upper end of the market segment to cover rising construction costs. Some of the supply of

for-sale housing is at risk of becoming subsumed into the rental market as investors are purchasing

single-family homes and converting them to rental units. The goal of the Michigan Homeownership

Study is to analyze, identify, and prioritize needs and gaps in the for-sale housing market. This study,

convened by MSHDA and conducted with the assistance of an Advisory Committee made up of key

stakeholders, aims to paint a regional and statewide picture of the housing landscape through

rigorous quantitative and qualitative data analysis and synthesis. The results will help affordable

MICHIGAN HOMEOWNERSHIP STUDY 13

housing industry decision makers adjust, add, or reconfigure existing housing programs to match the

needs of current and prospective home buyers across Michigan.

ROLE OF REPORT

This report is organized in two complementary pieces: the Michigan Homeownership Study and its

companion document the Michigan Homeownership Study: Key Trends and Measures by Prosperity

Region. The Michigan Homeownership Study document utilizes knowledge gained from extensive

data analysis and presents a series of thematic challenges, four municipal case studies, and a series of

strategies state, regional, and local leaders can use to advance homeownership opportunities.

Strategies are categorized by theme and identify potential challenges and opportunities for effecting

change. For each strategy we have identified which of the case study communities may benefit from

those policy changes and programs. The Michigan Homeownership Study document is intended to

be used by officials at all levels of government as an information and communication tool.

The companion document is a compilation of state and regional analyses relating to demographics,

socioeconomics, and housing. It identifies data points and highlights key findings by Prosperity

Region and statewide. The purpose of the companion document is to allow policy makers at the state

and regional level to understand the historical, current, and future challenges to the region related to

owner-occupied housing. The quantification of issues, especially those related to housing supply and

demand, are important for imparting regional change. The role of the companion document is to act

as a tool to educate leaders about the issues at the state and regional level. Please note that the terms

“affordable”, “obtainable” and “workforce” housing are generally used interchangeable throughout

the document to describe housing that is within the economic reach of households with about average

or below average incomes.

FRAMING OF THE ANALYSIS

Strategies in the document are

informed by a multi-level analysis of

demographic, socioeconomic, and

housing trends. The top-level

analysis involves looking at

Michigan in aggregate to understand

general trends and to provide a point

of reference for the regional analysis.

The second level of analysis is

conducted at the Prosperity Region

level. Prosperity Regions were

established and defined in 2013 to

foster greater regional cooperation

by leveraging existing resources and

opportunities. For this study, we

modified two of the Prosperity

Regions (Regions 2 and 10) to provide greater clarity on housing conditions in Detroit and Traverse

Figure 1: Map of Modified Prosperity Regions

MICHIGAN HOMEOWNERSHIP STUDY 14

City. The third level of analysis is the case studies which looks at four communities that could serve

as examples for other similar communities across the state.

PROSPERITY REGIONS

In 2013, Michigan defined ten Prosperity Regions which are made up of an agglomeration of counties.

For this study, modifications of two Prosperity Regions were made to provide greater clarity on

housing conditions. Prosperity Region Two was split into urban (Prosperity Region 2A) and rural

components (Prosperity Region 2B). Prosperity Region 10 was separated into the City of Detroit (10A)

and the rest of three county region (10B). This was done to ensure the uniqueness of the city’s housing

market was not lost amongst the regional story.

Conducting the analysis at the Prosperity Region level provided an understanding of the variety of

housing markets and conditions across the state. Regions are dynamic systems and are in part driven

by economic centers. Each region is different, some more urbanized with larger population and

employment centers and others more rural with less population and a different set of housing

challenges. Key takeaways were generated from each regional analysis which helped form the basis

for many of the strategies in this document. The accompanying Michigan Homeownership Study: Key

Trends and Measures by Prosperity Region Report contains the full analysis for each Prosperity

Region as well as a report for Michigan.

CASE STUDIES

To better understand how regional issues were manifesting in local communities, RKG presented the

Advisory Committee with a subset of cities from across Michigan that were representative of different

demographic, economic, and housing conditions. The Committee members selected by majority vote

four communities from this subset for these case studies. The resulting list of communities and their

respective community types chosen include:

• Urban Affordability – Grand Rapids

• Urban with Economic Challenges - Saginaw

• Aging Suburban - Westland

• Small Town Rural - Alpena

The case study analysis represents prototypical community typologies from across the state. The

Urban Affordability typology is applicable to urban communities experiencing significant

construction activity and price escalation, and where development or redevelopment is taking place.

The Urban with Economic Challenges case study highlights the challenges communities face when

the local economy declines, unemployment rises, local spending and tax revenues shrink, and

foreclosures, vacancy, and population loss take hold. The Aging Suburban case study looks at post-

war tract home subdivision communities with ranch-style homes built on a quarter acre lots, but have

not been modernized with upgraded systems or cosmetic changes that appeal to younger buyers in

today’s market. The Small Town Rural typology is intended to reflect geographically isolated

communities with small populations, fewer employment opportunities, and lower median household

MICHIGAN HOMEOWNERSHIP STUDY 15

incomes. Owner-occupied housing in these areas tend to be older and are primarily single-family or

manufactured homes.

Interviews with local officials, housing developers, and advocates, coupled with rigorous data

analysis allowed for an in-depth study. Lessons learned from the case studies were incorporated in

the strategies found at the end of this document.

Defining Affordability

Housing affordability can be defined as the relationship between household income and monthly

housing expenditures. A common measure of affordability is whether housing expenses exceed 30

percent of income. In that circumstance, a household is considered cost burdened and may be limiting

expenditures on other necessary purchases such as healthcare, childcare, education, or transportation.

Households in communities with escalating home prices face particularly acute challenges, as wages

are not keeping up with the rise in housing costs.

There are two common types of affordable housing in the marketplace today: deed restricted

affordable units and naturally-occurring affordable housing based on a community’s market prices.

Both types of affordable housing can serve a variety of needs. The crucial difference is that the market

determines the price of unrestricted affordable units, while a recorded legal instrument and strict

pricing guidelines determine the price of deed restricted units. This study does not differentiate

between deed restricted and unrestricted for-sale units, rather it looks at markets in totality to identify

needs and gaps that policymakers can choose to prioritize.

For this housing study, affordability is examined using Department of Housing and Urban

Development (HUD) Area Median Income (AMI) data which is based on specific geographies. For the

purposes of this study, we used AMI thresholds at the state, metropolitan region, and county levels.

The AMI data helps to inform purchase price affordability and is also used to compare existing supply

and future demand by price segment and household income. To understand the affordable/workforce

housing market, six AMI thresholds were analyzed for each study area:

• 30 percent of AMI

• 50 percent of AMI

• 80 percent of AMI

• 120 percent of AMI

• 200 percent of AMI

• Greater than 200 percent of AMI

The affordability gap between supply and demand is determined by comparing what is affordable at

each income threshold to what is available on the open market. Housing sales prices were collected

from across the state to determine median sales values by region.

MICHIGAN HOMEOWNERSHIP STUDY 16

OVERARCHING THEMES

Michigan’s homeownership market, much like the national market, constantly fluctuates. Ebbing and

flowing with the strength of the economy, shifting buyer preferences, and changes in the lending

environment. Since the Great Recession, many communities across Michigan have rebounded and are

seeing price increases that outpace what many potential homeowners can afford. In other

communities, challenging economic conditions, lower incomes, and a lack of investment in ownership

units have created a depression in the local market. In each community these issues surface in different

ways and require a wide range of tools that can be combined to stabilize the ownership market. Our

analysis of the homeownership market across Michigan and a scan of national trends in

homeownership revealed the following overarching themes.

Population, Wages and Purchasing Power

Homeownership continues to be a goal of many Michigan residents, but the pathways of achieving

this goal are becoming more difficult. Costs to build a new home or rehabilitate an older home

continue to rise, population and job growth in urban centers puts upward pressure on housing prices,

and households are saddled with more debt and fewer savings, making it more difficult to purchase

a home. Michigan’s population is projected to continue to increase, meaning new homes will need to

be built in hot markets and rehabilitation of older homes will need to be financed to support the

continued economic prosperity across the state.

POPULATION AND WAGES

Michigan’s population is projected to grow by 8 percent between now and the year 2045. Although

the trend line for growth over this time period is more stable than what may have been experienced

in previous decades, the state still needs to find ways of accommodating new residents in places they

want to live. The other challenge for Michigan is the ability to support more smaller households,

especially as the senior population continues to grow. More single-person households mean more

housing units, with the number of households projected to grow by 11 percent through the year 2045.

MICHIGAN HOMEOWNERSHIP STUDY 17

Like population and households, the number of jobs is projected to increase as well across Michigan.

Projections through the year 2045 show employment increasing by 4 percent, or 245,000 jobs.

Approximately one-third of those projected jobs are in sectors that tend to pay lower wages on

average. This includes food services, administration and support services, and local government. The

state’s median household income of $50,803 provides enough money to afford a house priced around

$175,000, yet the median sale price for a new single-family home in Michigan is just over $330,000.

New housing is not being built at price points that are affordable to the average Michigan household.

In 2018, food service and hospitality workers earned an average of $23,150 per year, which is enough

to purchase a home valued at $75,000. Not all projected jobs are lower wage earners, though. A third

of all employment growth is expected in the professional and technical services sector, which has an

average wage of more than $100,000.

A.L.I.C.E. POPULATION

Michigan has nearly 3.8 million households, of which 15 percent lived in

poverty and 25 percent are categorized as Asset Limited, Income

Constrained, Employed (ALICE), which refers to working households that

do not earn enough to cover all household needs. ALICE households are

those on the edge of poverty. These households have very little cushion in

their paycheck or savings to cover increases in costs, particularly housing

costs. Every day costs continue to rise, making it more difficult for ALICE

households to afford housing, transportation, food, education, and healthcare. According to a 2017

ALICE report for Michigan, nearly two-thirds of all jobs across the state paid less than $20 per hour,

which is not enough to support a family of four.

1

Over the next five to ten years, low-wage jobs are

1

2017 ALICE Update, United Ways of Michigan.

Figure 2: Michigan Historical and Projected Population, 1970 - 2045

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

1970 1980 1990 2000 2010 2016 2017 2018 2019 2020 2025 2030 2035 2040 2045

Michigan Historical and Projected Population, 1970 - 2045

Source: REMI

Michigan

MICHIGAN HOMEOWNERSHIP STUDY 18

projected to increase at a faster rate than high-wage jobs, making affordable housing for working

households even more critical. When we talk about the workforce and obtainable housing, it is

important to consider housing options for working households that are earning at or below 80

percent of the area median income. This is a very different economic situation than the more

traditional definition of workforce housing for households in the 100 to 140 percent of area median

income range.

LIMITATIONS TO PURCHASING POWER

In addition to housing prices outpacing wage growth across many sectors, home buyers are also

challenged by increased debt, fewer savings, and stricter lending requirements. This is particularly

true for younger households looking to enter the homeownership market. A recent study by

researchers at Apartment List estimated that millennial buyers are facing an uphill battle to save

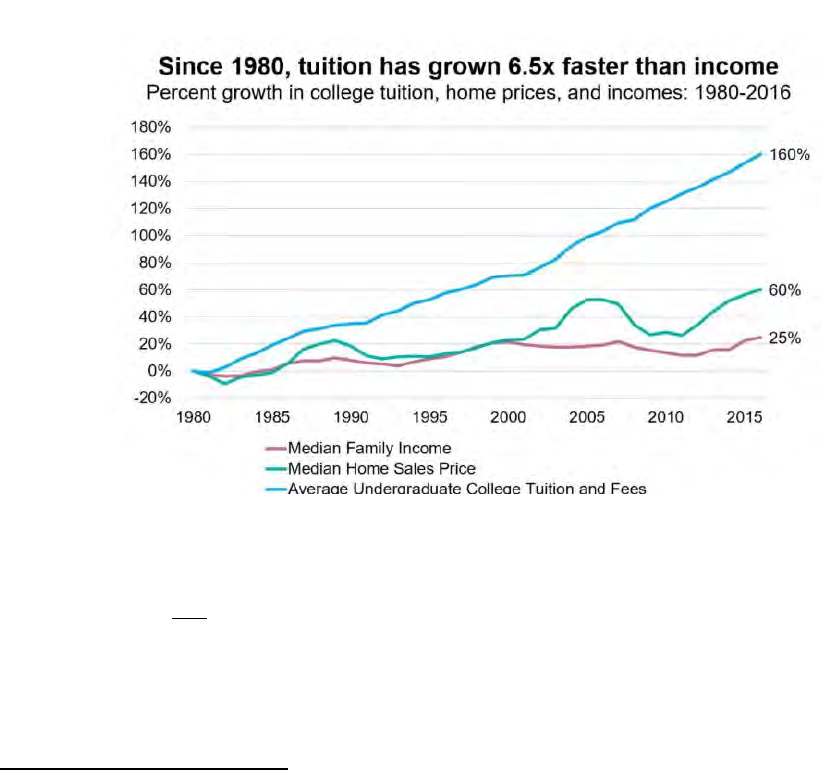

enough money for a down payment with the added debt load of student loans. Since 1980, tuition

rates have grown 6.5 times faster than incomes with average undergraduate tuition rates increasing

160 percent since 1980.

2

The study estimates millennials with college debt will require an average of 12 years to save up for a

20 percent down payment compared to only 7.6 years for graduates without debt. This comes at a

time when tuition and housing prices continue to rise. This generation represents the next big wave

of potential homebuyers and provides a way out for senior households looking to down size. If

purchasing power is limited and renting becomes a longer-term trend, turnover in the ownership

market may be impacted. Finding ways to increase access to quality housing through financial

2

Student Debt and Millennial Homeownership. January 2018. https://www.apartmentlist.com/rentonomics/student-debt-

millennial-homeowership/

Figure 3: National Trend of Wages, Homes Prices, and Tuition

MICHIGAN HOMEOWNERSHIP STUDY 19

assistance, rehabilitation assistance, or deed restricted affordable housing will be important going

forward.

Housing Inventory

The ongoing maintenance and expansion of the housing stock is vital for maintaining healthy

neighborhoods and communities. Over the last seventy years, Michigan experienced both a rapid

growth and decline in households. During the immediate post-war period, job opportunities in the

manufacturing sector were a magnet for household growth. New suburbs were built in communities

across the state to house families leaving urban areas or relocating from other parts of the country.

This period of growth tapered off in the 1980’s, and a long-term decline soon followed due to

structural changes in the economy. During the downturn, losses in households resulted in excess

housing supply and rising vacancy rates. Today, a housing imbalance exists where some communities

are growing and seeing price appreciation, while others are experiencing population loss and declines

in home prices

PUSH TOWARD HIGHER END HOUSING PRODUCT

Housing market momentum tends to build in locations where developers can realize the greatest

financial return and experience minimal risk exposure. One of the findings from this housing study is

that new construction has pivoted towards the upper end of the income spectrum. Developers are

building homes (both single-family and condominiums) at price multiples much greater than what an

average household can afford. Amenities offered include larger sized units, luxury finishes, and

building amenities. Comparatively, the existing housing stock does not offer such features as much of

it was built for working class families at a time when these luxury features were less common.

From a pricing perspective, there is nearly a $100,000 sales price differential between existing and new

homes in Michigan. The price gap between existing and new homes has shrunk over time, as sales

prices for existing homes rose 70 percent since 2012. In many circumstances, purchasing a new home

makes more sense from a homebuyer’s perspective as new homes are move-in ready, require no

upfront rehab work, and come fully equipped with modern appliances and systems. The challenge in

Michigan is how to raise the quality of the existing housing stock to provide affordable

homeownership opportunities that are enticing to new buyers.

MICHIGAN HOMEOWNERSHIP STUDY 20

MISSING MIDDLE

Across Michigan there are three primary housing markets: those below 80 percent of AMI, those

between 80 percent and 120 percent of AMI, and those earning more than 120 percent of AMI. The

graph below presents affordable sales prices across all AMI thresholds in comparison to market

pricing. From the data, households below 80 percent of AMI cannot afford existing homes priced at

or above the median sales value. Conversely, for households with incomes above 120 percent of

AMI, housing choice exists. These households have the option to purchase existing housing units, or

new units, depending on what they can afford.

Figure 4: Sales Price of New Housing Units

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

2012 2013 2014 2015 2016 2017 2018

Sales Price

Median Sales Price Across Michigan, 2012 - 2018

Source: MLS

Existing Single Family New Single Family Existing Condo New Condo

MICHIGAN HOMEOWNERSHIP STUDY 21

Missing middle housing is a potential supply side solution for those households earning between 80

percent and 120 percent of AMI. In many parts of the state, the missing middle market is where

housing options are most limited. Households in this category have the financial means to purchase

existing housing units but not enough income to purchase new housing product. This disconnect

within the marketplace results in greater demand for quality housing product located in desirable

communities or neighborhoods. The increase in overall demand results in price escalations across the

entire housing stock and contributes to the lack of affordability. In many communities, zoning

regulations restrict residential density, particularly in single-family neighborhoods so that new

housing at greater densities are not built.

One way to address the gap in missing middle housing is to increase residential densities, product

diversity, and a range of price points in established neighborhoods. By facilitating the development

of infill developments, communities can add new product types such as duplexes, three-family, and

small multifamily (5-10 units) developments. These lower-priced units can offer an entry point for

households looking to purchase homes and establish roots within a community.

One of the methods to actualize change is to update local zoning ordinances to remove single-family

zoning. Minneapolis recently updated its zoning ordinance across the city to end single-family zoning.

The intent of the update is to allow for greater diversity of housing types within existing

neighborhoods.

3

The change was heralded as a step toward addressing housing affordability and

equity, with greater housing diversity augmenting the supply of housing to meet demand. Similarly,

3

https://www.nytimes.com/2018/12/13/us/minneapolis-single-family-zoning.html

Figure 5: Maximum Purchase Price Based on Median Income in Michigan

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

30% AMI 50% AMI 80% AMI 120% AMI 200% AMI

Sales Price

Maximum Purchase Price Based on Median Income in Michigan

Source: HUD, MLS

Affordable Single-Family Affordable Condo Existing Single-Family

Existing Condo New Single-Family New Condo

MICHIGAN HOMEOWNERSHIP STUDY 22

about ten years ago Grand Rapids implemented a form-based code across certain parts of the city

which increased housing diversity.

4

The results from Grand Rapids are promising and may offer a

pathway to communities facing issues of price escalation and limited developable land.

REHABILITATION

In aggregate, Michigan has large numbers of homes which are vacant or in need of repair. As a result

of population and household declines during the 1980’s, many communities were left with

neighborhoods or areas experiencing high levels of unemployment and underinvestment in the

housing stock. Over time, some communities were able to rebound from the decline and pivot to

towards revitalization, while others have turned the corner.

Large scale rehabilitation of the housing stock is difficult to execute because it requires a concerted

effort on the part of homeowners, the availability of financing, and coordinated efforts by municipal

officials. Rehabilitation is difficult from the homebuyer side because financial capital is not always

readily available for renovation projects. While some lenders offer construction financing, lending

terms may not be favorable to low- to moderate-income households who are unable to pay the loan

back on top of an existing mortgage. While there are state and local programs which help homeowners

finance rehabilitation costs, these funds are limited.

The location of properties also plays a significant role in home renovation financing. In rural areas

where comparable appraisals are fewer in number, lenders tend to be unwilling to provide funds for

acquisition and renovation. This is due to the risk associated with investing in properties which are

not located in active housing markets, and the general risk-averse nature of lenders today. In markets

with greater real estate activity, lenders are more willing to invest, but mostly with individuals who

can afford to undertake the rehab project. One of the key challenges for low-to moderate-income

households is accessing financing to undertake rehabilitation projects and open up housing choices

that are more affordable than purchasing new homes.

Development Costs

One of the themes that rose to the top during the interviews with housing experts across Michigan

was the cost of building as a driver of price increases. Challenges related to construction industry

jobs, labor shortage, rising wages, and material costs permeated our conversations. Availability of

skilled labor in the construction industry is a major issue in Michigan but also across our nation as

more young people attend college and enter more technical fields. At the same time, material costs,

land values, and permitting times have increased in many locations, adding to the builder’s hard

and soft costs making it more challenging to offer an affordable product to potential buyers.

LABOR AND CONSTRUCTION

One of the contributing factors to the rise in new home prices across parts of Michigan is the

shortage of construction labor. Between 2001 and 2010, Michigan lost just over 89,000 construction

sector jobs as a result of the Great Recession, a major slow down in construction activity, and a shift

of the workforce to other employment sectors. Interviews with housing experts revealed a

4

https://nextcity.org/daily/entry/a-decade-without-single-family-residential-zoning-in-grand-rapids

MICHIGAN HOMEOWNERSHIP STUDY 23

significant migration of construction workers to more prominent markets in the south and

southwest where labor was in-demand and construction was booming. Since 2010, the construction

labor market as started to come back, gaining back about half the jobs that were lost in the previous

decade. That trend is expected to continue, but labor shortages will still prevail as Michigan is not

projected to reach 2001 employment levels even by the year 2028.

In addition to rising labor costs, the National Association of Home Builders (NAHB) has noted

increasing permitting costs and extended approval time periods are also attributing to the rising cost

of housing. Nationally, 25 percent of the cost of a typical home can now be attributed to

development reviews, mitigation studies and reports, site plan revisions, architectural plans, and

permitting fees.

5

These delays flow down into the builders’ bottom line and eventually passed on to

the buyer.

5

Housing Challenges Threaten Our Economic Growth. Home Builders Association of Michigan, June 2017.

Figure 6: Construction Industry Job Change

MICHIGAN HOMEOWNERSHIP STUDY 24

PRODUCT DELIVERY

The increase in costs and challenges with

labor availability have created a situation for

many home builders where it is more cost

effective to build fewer homes per year but

make them larger and more expensive to

make up for losses in volume. In many of

Michigan’s prominent housing markets such

as Traverse City, Grand Rapids, Ann Arbor,

and parts of Downtown Detroit, prices for

new housing units continue to escalate at a

far faster rate than the existing housing stock

creating a situation where new units are no

longer available to most Michigan households.

For example, in Grand Rapids new single-family homes sold in 2018 had an average sales price of

$300,000 compared to existing homes that sold at an average of $153,000. The combination of rising

costs, scarcity of product, and demand to live in Grand Rapids are all causing new homes to sell for

nearly twice the price of an older existing home. The same trends can be seen in the new

condominium development and rehab projects in Downtown Detroit. Condominiums built between

2010 and 2018 had an average sales price of $444,400, which compares to condos built between 1990

and 2010 which sold for an average of $178,500. That equates to a 150 percent higher selling price for

newer condo units. With sales prices for new product continuing to rise, the focus for more

affordable housing options lies within the existing housing stock, which in many cases needs

rehabilitation and upgrades to be saleable in today’s homeownership market.

Barriers to Homeownership

Accessing the home ownership market offers a pathway to building longer-term equity and wealth,

but entering the world of home ownership and finding an asset that has appreciating value is

becoming more challenging. Local regulations, market conditions, and the ability to afford a quality

home are challenges not only in Michigan’s market but in many places across the country.

REGULATORY

Local zoning regulations and permitting processes can add time and risk to the approval and

construction of residential units. Zoning restrictions that limit density, create large lot subdivisions,

and limit product type can upset the supply and demand balance particularly in a market where

housing demand is high. Continued layering of building code regulations, while good practice, can

also lead to increased construction costs that are eventually passed on to the buyer through higher

sale prices. Municipalities should look at their local market, understand their current housing supply,

and tailor zoning regulations to meet the market for both ownership and rental housing options.

LENDING REQUIREMENTS

As a response to the housing market crash and Great Recession, lending requirements for mortgages

were tightened to ensure that lenders were not providing mortgages to buyers who could not afford

New condo building in Detroit. Source: Redfin

MICHIGAN HOMEOWNERSHIP STUDY 25

it. This meant increased down payment amounts, enhanced credit scores, and ensuring loan-to-value

ratios were in line. As we have seen nationally, first time home buyers are coming in with more debt

than ever before between student loans, credit cards, and other accumulated debt obligations. Paying

down debt obligations has led to fewer households with adequate savings to meet down payment

requirements, and challenges with maintaining a qualifying credit score. A 2018 report from the

Federal Reserve showed that 40 percent of adults could not cover a $400 unexpected expense if one

arose.

6

As student loans and housing prices continue to rise, saving more money for a home purchase

will become more difficult.

The other challenge for home buyers in Michigan is the ability to obtain financing for acquisition and

rehabilitation for older homes that need work either due to deferred maintenance or changes to make

the home more livable. In some markets across Michigan it can be challenging for the lender to find

comparable properties that justify an appraisal value that covers both the sale price and rehabilitation

costs for the home. For example, if a buyer purchases a home for $75,000 and must put another $40,000

into rehabilitation, the home may not appraise for $115,000 if there are not comparable properties in

the area. The loan-to-value ratio ends up being too high and leaves the buyer with a financing gap

typically on the rehabilitation side of the loan. If the buyer cannot come up with another source of

financing, it can be very difficult to get a loan. This issue is particularly pertinent to Michigan as there

are many existing homes across the state that could serve as affordable and obtainable ownership

options but need rehabilitation to make them livable and/or marketable to buyers.

MARKET STRENGTH

Investment in new ownership construction and rehabilitation projects are not evenly disbursed across

Michigan. There are markets where construction is booming, and buyers are competing to find

ownership units. There are also markets where home values are declining, and vacancy grows. There

are many factors driving the decisions of developers and buyers which include access to jobs,

transportation connectivity, quality schools and services, natural features, and amenities. There is also

a desire, particularly for younger and older residents, to be in or near activity centers and major cities.

These places offer greater economic opportunity, cultural activity, diversity, housing choice, and retail

and restaurant amenities. Communities that can put forward a competitive package of attributes will

do well, those that cannot may continue to decline. Finding the right strategies to incentivize

investment in softer markets will be important in stemming the loss of population in some markets

and providing employers with the support they need to attract workers.

6

Fed Survey Shows 40 Percent of Adults Still Can’t Cover a $400 Expense. CNBC, May 22, 2018.

https://www.cnbc.com/2018/05/22/fed-survey-40-percent-of-adults-cant-cover-400-emergency-expense.html

MICHIGAN HOMEOWNERSHIP STUDY 26

CASE STUDIES

Opportunities and challenges within the homeownership market are impacted by broader trends that

occur at the national and state level, but it is at the municipal level where change is seen and felt.

Michigan has a wide variety of community types each with their own challenges when it comes to

furthering obtainable homeownership opportunities. Growing urban communities face challenges of

rising home values and displacement while economically-challenged urban communities are dealing

with population decline and vacancy issues. Prospering suburbs are facing new growth pressures and

struggling with how best to repurpose land to meet today’s housing demands. Rural communities

struggle to retain younger residents to fill jobs and purchase homes, yet some see increases in seasonal

population and a loss of year-round housing stock to the second home market.

While each of Michigan’s 1,773 cities, villages, and townships are unique, this document uses a case

study approach to communicate potential challenges and solutions that may be applicable to a broader

range of communities. For example, the City of Ann Arbor may fall into the Urban Affordability

category based on similar demographic, economic, and market trends to that of Grand Rapids. The

same could be said for the City of Royal Oak which could fall into the Aging Suburban category with

similar characteristics to the case study community of Westland. The four case studies highlight trends

and market considerations for each place type and offer some insights on the opportunities and

challenges in the homeownership market.

Urban Affordability – Grand Rapids

In many urban communities across the country, housing affordability has become a major challenge

and is impacting residents and businesses alike. In some locations, the cost of renting or owning a

home far out paces incomes. The mismatch in the marketplace between prices and affordability has

been exacerbated by low costs to borrow money and a building cycle which has pushed developers

to build more units with top of market price points. The Urban Affordability typology is applicable to

urban communities experiencing significant construction activity and price escalation, where

development or redevelopment is taking place along commercial corridors, in areas served by public

transportation, and neighborhoods that provided opportunities for low- and middle-income

households to live affordably.

Credit: Experience Grand Rapids

MICHIGAN HOMEOWNERSHIP STUDY 27

DEMOGRAPHICS

Grand Rapids is a growing city. Over the last ten years, total population grew by 2 percent as

compared to the state’s overall population which did not increase at all.

7

However, what is

particularly telling is that residents ages 25-34 increased by 15 percent over the same period. Driving

some of this change is the fact that Grand Rapids is home to fifteen higher education institutions in

the metro area with a combined 40,000 students. Some of these students may be staying in the city

after school for job opportunities. This population has drawn the interest of developers and investors

and created a market for the new development across the city. Neighborhoods like Downtown and

the West Side have seen new apartments, condos, and mixed-use developments which include stores,

restaurants, and other amenities catering to young professionals and retirees alike.

At the same time, the number of residents ages 55 and older is growing. Between 2011 and 2016, the

City saw an increase of 11 percent in this population cohort. The population changes and economic

opportunities in Grand Rapids have provided the impetus for developers to invest in new multi-

family rental and condo buildings. Market preferences for both younger and older residents are

aligning with interest in managed buildings, no maintenance, elevator access, covered parking, and

neighborhood amenities in walking distance.

INCOMES AND EMPLOYMENT

7

American Community Survey 2007-2011, 2012-2016, Table B01001, 2018

Figure 7: Change in Population by Age

-3%

0%

15%

-3%

-13%

16%

7%

-3%

2%

7%

-5%

-6%

16%

17%

-6%

2%

3%

-10%

-8%

12%

14%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Under 18 18 to 24 years 25 to 34 years 35 to 44 years 45 to 54 years 55 to 64 years 65+ years

Percent

Change in Population, 2011-2016

Source: ACS

Grand Rapids Prosperity Region Four Michigan

MICHIGAN HOMEOWNERSHIP STUDY 28

Even though employment has increased in Grand Rapids, median household income continues to fall

behind the state’s median. In Grand Rapids, the median household income is $42,019 compared to the

state median of $50,803.

8

Since 2011, there has been a shift toward higher income households with

incomes between $75,000 and $100,000 growing by 10 percent. There has also been a decline in the

number of households earning less than $50,000. This could be a combination of upward mobility and

potential displacement of lower-income households from Grand Rapids.

Grand Rapids is a large employment center within Prosperity Region Four with three industry sectors

comprising nearly 50 percent of the total jobs in the city. These industry sectors include: Health Care

and Social Assistance (26 percent), Manufacturing (13 percent), and Administration & Support (10

percent).

9

The largest employer in the area is Spectrum Health with nearly 25,000 employees. This

health system employs a variety of medical professionals and offers competitive wages. Local

manufacturing firms include companies like Steelcase which employs 2,000 workers.

10

Additionally,

there are large manufacturers outside of the city in the nearby communities of Zeeland, Holland, and

Muskegon with corporate headquarters for Herman Miller and Gentex.

8

American Community Survey 2007-2011, 2012-2016, Table B19013, 2018

9

OTM, 2018

10

https://www.steelcase.com/find-us/locations/americas/grand-rapids-michigan/

Figure 8: Change in Household Income

-11%

-4%

-9%

-3%

6%

10%

16%

36%

-8%

-8%

-4%

-3%

3%

4%

17%

36%

-3%

-3%

-2%

-2%

0%

0%

7%

24%

-20%

-10%

0%

10%

20%

30%

40%

Less than

$15,000

$15,000 -

$24,999

$25,000 -

$34,999

$35,000 -

$49,999

$50,000 -

$74,999

$75,000 -

$99,999

$100,000 -

$149,999

$150,000 or

more

Percent

Change in Household Income, 2011-2016

Source: ACS

Grand Rapids Prosperity Region 4 Michigan

MICHIGAN HOMEOWNERSHIP STUDY 29

HOUSING MARKET

Since 2011, the housing market in Grand Rapids has seen a shift in ownership patterns with the share

of owner-occupied homes declining by 6 percent, compared to the region and state at 1 and 3 percent,

respectively.

11

At the same time, renter-occupied housing has increased by 8 percent. Vacant

properties experienced a dramatic decline over the last decade with a decrease of 21 percent. This drop

in vacancy speaks the desirability and strength of the city’s housing market. The overall increase in

rental units a result of a combination of new apartment construction around Grand Rapids, and the

ever-increasing occurrence of single-family homes which were once ownership units being converted

to rental units.

Table 1. Housing Units

Tenure

Grand Rapids Grand Rapids Prosperity Region Four Michigan

2011

2016

Change

% Change

% Change

% Change

Owner-Occupied 42,025 39,655 -2,370 -6% -1% -3%

Renter-Occupied

31,064

33,413

2,349

8%

10%

11%

Vacant

8,471

6,651

-1,820

-21%

-5%

-3%

Total 81,560 79,719 -1,841 -2% 1% 0%

Source: American Community Survey 2007-2011, 2012-2016, Table B25003, 2018

AGE OF STRUCTURE

Grand Rapids has an older housing stock when it comes to ownership units. Nearly 68 percent of

owner-occupied structures were built before 1959, and only 5 percent were built after the year 2000.

12

However, recent trends show that between 2007 and 2016 there was a 25 percent increase in the

number of homes built after 2000. This far outpaces the change experienced across both the region

and state, which had growth of 17 percent and 14 percent, respectively.

OWNER-OCCUPIED HOME PRICES

The median price of a single-family home in Grand Rapids increased 114 percent between 2012 and

2018. This drastic price escalation has had an impact on affordability for existing residents, particularly

for those with incomes below the median. Figure 9 compares the price of new single-family homes

and condominums to those that already existed in the market by year sold. Between 2011 and 2016,

the median sale price for existing owner-occupied units increased to the point where a household

earning the median income could not longer afford a home selling at the city’s median value. New

ownership units entering the market substantially exceed what a household earning the median

income could afford. For example, sale prices for new condominiums jumped 67 percent from 2011 to

2016.

11

American Community Survey 2007-2011, 2012-2016, Table B25003, 2018

12

American Community Survey 2007-2011, 2012-2016, Table B25036, 2018

MICHIGAN HOMEOWNERSHIP STUDY 30

PRICING BY YEAR BUILT

Between 2012 and 2018 there were 19,700 sales with a median price of $145,142.

13

Home sales of

structures built between 1900-1950 were the most numerous, and offer housing at a price point that is

more affordable to homebuyers in Grand Rapids. Although the units may need improvements, the

relatively low price point allows buyers with low to moderate incomes an entry point for

homeownership. Not surprisingly, home prices increase as the age of the home decreases. For

example, the difference in price between a single-family home built between 1990-2010 compared to

one built between 2010-2018 is about 28 percent. Newer homes have updated heating and cooling

systems, modern insulation, and friendler layouts that are generally more attractive than older homes.

The condominum market in Grand Rapids has seen a sharp escalation in pricing, particularly for units

built after 1990. The difference in price between a condomium built between a condominum built

between 1990-2010 and one built between 2010-2018 is about 30 percent.

13

Multiple Listing Service (MLS) Data, Michigan Board of Realtors, RKG Associates, 2018

Figure 9: Median Owner-Occupied Sales Price

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

2012 2013 2014 2015 2016 2017 2018

Sales Price

Grand Rapids Median Sales Prices, 2012 - 2018

Source: MLS

Existing Single Family New Single Family Existing Condo New Condo

Home price

affordable to

household at

median income

MICHIGAN HOMEOWNERSHIP STUDY 31

DEVELOPMENT PIPELINE

As was noted earlier, Grand Rapids is seeing a lot of new residential and mixed-use development in

certain neighborhoods across the city. Currently, a majority of the new residential projects are rental

and not homeownership although some new condominiums are going up. In 2018, a new mixed-use

development was completed on the West Side that included a food market concept. Bridge Street

Market is a new 37,000 square foot store that offers fresh and locally sourced artisanal products and

anchors a new mixed-use development. The Hendrik, a new mixed-use building contains 116

apartments and nearly 56,000 square feet of office space.

14

On the homeownership side, the Viridian Place condominium development was recently approved

in Northeast Grand Rapids. This development will include 130 condominium units spread across

twenty-five two-story buildings. Each building will consist of 2, 4, 6 or 8 dwelling units.

15

HOMEOWNERSHIP CHALLENGES IN GRAND RAPIDS

DEMAND FOR RENTAL UNITS

Demand for housing in Grand Rapids has been strong over the last decade, however developers are

building many more rental units than ownership units. Trends in homeownership, affordability, and

the general economics of housing development are driving preferences to build more rental housing.

14

https://www.mlive.com/news/grand-rapids/index.ssf/2018/08/shoppers_thrilled_as_meijer_un.html

15

https://www.mlive.com/news/grand-rapids/index.ssf/2018/04/134-unit_condominium_proposal.html

Figure 10: Median Owner-Occupied Sales Price by Year Built

$68,900

$97,699

$136,500

$158,560

$164,247

$210,304

$205,563

$181,475

$86,920

$108,675

$217,250

$283,350

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

Before 1900 1900 - 1950 1950 - 1970 1970 - 1990 1990 - 2010 2010 - 2018

Sales Price

Grand Rapids Median Sales Price by Year Built, 2011-2016

Source: MLS

Single Family Condo

MICHIGAN HOMEOWNERSHIP STUDY 32

Condominiums can be more difficult for developers to finance in today’s lending market and can be

more challenging for owners to obtain a mortgage to purchase due to criteria imposed by lenders.

With the development focus shifted toward redevelopment and infill projects, the market for new

homeownership units in Grand Rapids may trail behind rental units for some time.

LACK OF SMALL-SCALE DEVELOPMENT

Incentives for smaller-scale condo and townhome-style units are harder to come by in Grand Rapids.

Housing for the so-called “missing middle”, smaller-scale multi-unit housing types such as duplexes,

fourplexes, bungalow courts, and converted single-family homes, are not being built at the same pace

as larger multi-family structures.

16

In order to encourage this type of development, simplifying the

review process and modifying current site layout and building placement standards has been

proposed. Changes to residential zoning districts in Grand Rapids has provided some opportunities

for developers to build multi-family style housing in existing single-family neighborhoods. While this

proposal would increase overall density within neighborhoods, it would help address housing supply

issues for smaller-scale homeownership opportunities.

FHA APPROVED CONDOMINIUM ASSOCIATIONS

The FHA Spot Loan Approval Process was eliminated in 2010 which restricted lenders from offering

FHA loans on individual condominiums. New regulations require condominium associations to

become certified by HUD for buyers to utilize FHA backed loans. The certification must be renewed

every two years. The result of this process has been a lack of FHA approved condominium complexes

which accept FHA loans. Of all the condominium developments in Grand Rapids, there are only five

complexes totaling 715 units which are currently approved for FHA loans.

16

https://www.grandrapidsmi.gov/Directory/Programs-and-Initiatives/Housing-NOW

MICHIGAN HOMEOWNERSHIP STUDY 33

Urban with Economic Challenges - Saginaw

Communities experience economic ebbs and flows resulting in periods of growth and decline. In some

cases, national trends such as recessions have short-term implications which limit local growth and

cause hardship for the population, but these downturns tend to be temporary and communities

ultimately recover to varying degrees. However, there cases in which communities experience

prolonged economic downturns as a result of structural changes in the local and regional economy.

This situation is more likely to occur in communities centered around a single industry sector that is

declining or a large employer that leaves the area.

The Urban with Economic Challenges case study highlights the challenges communities face when

the local economy declines, unemployment rises, local spending and tax revenues shrink, and

foreclosures, vacancy, and population loss take hold.

DEMOGRAPHICS

The City of Saginaw serves as the case study for an urban community with economic challenges.

Saginaw’s economy relied on the manufacturing industry for decades, but the shift of production to

offshore locations created a period of rapid decline with the City’s population cut in half between 1960

and 2016. A city with a population of nearly 50,000 is facing the challenges of population loss,

economic decline, and a housing stock where one in five units sits vacant.

Demographic trends in Saginaw show the population shrinking and getting older. Between 2011 and

2016, population has declined another 5 percent or 2,633 people.

17

The city experienced a decline

across nearly all age cohorts, except for those ages 55 years and older which saw an increase of 8

percent. The growing senior population is a concern for the City as they have limited housing choices,

may not be able to maintain their single-family home, and do not have much equity in their home as

Saginaw home prices are relatively low.

17

American Community Survey 2007-2011, 2012-2016, Table B01001, 2018

Credit: Saginaw Art Museum

MICHIGAN HOMEOWNERSHIP STUDY 34

One of the most striking findings is that the population between 25 and 34 decreased by 12 percent

versus the region and state which saw increases. Younger residents in Saginaw who leave for college

or job opportunities elsewhere are not returning to the City later in life. The decline in this age cohort

can also make it difficult to attract new employers to the area or retail and service-based businesses

looking for households with expendable income.

INCOMES AND EMPLOYMENT

The median household income in Saginaw is $28,871 which is about half as much as the state’s

median.

18

Between 2011 and 2016, median income fell by 3 percent. Figure 12 shows the change in

household income by category from 2011 to 2016. Households in the highest income bracket decreased

by 39 percent, yet at the same time there was a 39 percent increase in the percent of households within

incomes between $75,000 and $99,999 raisin from 972 households to 1,351 households.

19

Some of the

shifts in income are the result of higher income households leaving the area, while new job

opportunities in the healthcare sector have brought in new upper middle-income households.

18

American Community Survey 2007-2011, 2012-2016, Table B19013, 2018

19

American Community Survey 2007-2011, 2012-2016, Table B19001, 2018

Figure 11: Change in Population by Age

-14%

2%

-12%

-4%

-5%

8%

7%

-8%

-3%

4%

-11%

-10%

9%

12%

-6%

2%

3%

-10%

-8%

12%

14%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Under 18 18 to 24 years 25 to 34 years 35 to 44 years 45 to 54 years 55 to 64 years 65+ years

Percent

Change in Population, 2011-2016

Source: ACS

Saginaw Prosperity Region 5 Michigan

MICHIGAN HOMEOWNERSHIP STUDY 35

The healthcare and manufacturing sectors continue to dominate Saginaw’s market comprising 59

percent of all jobs.

20

Major employers in the area include Nexteer Automotive, Covenant Healthcare,

St. Mary’s of Michigan, and Morley Companies. These companies alone employ over 12,000.

21

In

nearby Midland, Dow Chemical has its headquarters which serves the region as a major employment

hub.

HOUSING MARKET

Since 2011, the housing market in Saginaw has experienced 2 percent decline in the number of owner-

occupied units, which is similar to that of the region and state. At the same time, the number of renter

households increased by 4 percent. The city’s ownership housing stock is dominated by single-family

structures, comprising nearly 98 percent of all ownership units. Vacant properties are a major issue in

Saginaw, with 20 percent of all housing units listed as vacant. The City has focused its efforts on

reducing vacant and blighted structures through a systematic demolition program which helped

remove 860 vacant homes between 2013 and 2015.

22

20

OTM, 2018

21

https://saginawfuture.com/data-demographics/primary-employers/

22

https://www.mlive.com/news/saginaw/index.ssf/2016/10/saginaw_gets_22_million_to_con.html

Figure 12: Change in Household Income

-4%

-6%

8%

13%

-14%

39%

8%

-39%

-3%

-5%

1%

-3%

-2%

6%

8%

18%

-3%

-3%

-2%

-2%

0%

0%

7%

24%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Less than

$15,000

$15,000 -

$24,999

$25,000 -

$34,999

$35,000 -

$49,999

$50,000 -

$74,999

$75,000 -

$99,999

$100,000 -

$149,999

$150,000 or

more

Percent

Change in Household Income, 2011-2016

Source: ACS

Saginaw Prosperity Region 5 Michigan

MICHIGAN HOMEOWNERSHIP STUDY 36

Table 2. Housing Units

Tenure

Saginaw Saginaw Prosperity Region Five Michigan

2011 2016 Change % Change % Change % Change

Owner-Occupied

12,025

11,790

-235

-2%

-2%

-3%

Renter-Occupied 7,378 7,639 261 4% 5% 11%

Vacant

5,357

4,888

-469

-9%

-1%

-3%

Total 24,760 24,317 -443 -2% 0% 0%

Source: American Community Survey 2007-2011, 2012-2016, Table B25003, 2018

AGE OF STRUCTURE

Saginaw has an older housing stock when it comes to ownership units. Nearly 77 percent of owner-

occupied structures were built before 1959, and only 1 percent were built after the year 2000.

23

Between 2011 and 2016 there was a 20 percent decrease in the number of new homes built. The local

market in Saginaw fell far below the region and state, which had growth of 18 percent and 14 percent,

respectively.

OWNER-OCCUPIED HOME PRICES

The median price of a single-family home in Saginaw decreased by 14 percent between 2012 and 2018.

In 2012, the median sales price of a single-family homes was $40,700 and in 2018 the median sales

price decreased to $35,000. Condominium prices also experienced a drop in median sales price, falling

18 percent over the same period. Figure 13 compares the price of new single-family homes and

condominums to those that already existed in the market by year sold.

PRICING BY YEAR BUILT

Between 2012 and 2018 there were 7,700 home sales with a median price of $37,732.

24

Homes sales of

structures built between 1900-1950 were the most numerous with 3,153 and a very low median sales

price of $20,505. This compares to sales of homes built between 1990 and 2010 where the median sales

price was $151,465. While the newer homes built after 1990 are selling for nearly 6.5 times are much

as homes built before 1950, the older units likely need substantial structural and cosmetic upgrades.

The condominum market in Sagniaw has seen a continuation in price escalation, however very few

units are changing hands as compared to single-family homes. In each of the respective year built

categories, prices have nearly doubled as time progressed.

23

American Community Survey 2007-2011, 2012-2016, Table B25036, 2018

24

Multiple Listing Service (MLS) Data, Michigan Board of Realtors, RKG Associates, 2018

MICHIGAN HOMEOWNERSHIP STUDY 37

Figure 13: Median Owner-Occupied Sales Price

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

2012 2013 2014 2015 2016 2017 2018

Sales Price

Saginaw Median Sales Prices, 2012 - 2018

Source: MLS

Existing Single Family New Single Family Existing Condo New Condo

Home price

affordable to

household at

median income

Figure 14: Median Owner-Occupied Sales Price by Year Built

$12,875

$19,810

$45,540

$86,900

$154,980

$58,300

$15,408

$21,200

$37,800

$65,880

$147,950

$227,277

$0

$50,000

$100,000

$150,000

$200,000

$250,000