Is your digital

future in the

right hands?

An annual review of the real

estate industry’s journey into

the digital age

KPMG Global PropTech Survey

October 2019

kpmg.com/realestate

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Introduction

The real estate industry is still making progress with its digital

transformation. Challenges remain, however, with full-scale

adoption of digital technology still some way off.

In its third year, the annual KPMG Global PropTech survey looks at the progress made in

the real estate industry’s relationship with technology over the past year. We examine the

differences between regions, industry sub-sectors and stages of the property cycle, and we

explore the areas in which attitudes and practices may need to change. We also focus on

the crucial questions of who has responsibility for advancing the digital agenda and whether

companies have the talent in place to deliver the job.

All in all, the developments of the past year are encouraging. Property companies

are increasing their engagement with digital, and many companies are taking digital

developments in their stride. Brokers and advisors, in particular, are at the forefront of the

technological revolution, with automation and digitalization playing a growing part in their day-

to-day operations.

At the same time as they embrace digital transformation, companies are putting more

emphasis on data. They are increasingly keen to explore the ways in which it can revolutionize

their operations and – importantly – improve the experience of their customers.

The digital revolution brings challenges, of course. Cyber security is an issue of rapidly

growing importance – an issue that real estate companies are increasingly acknowledging. In

the survey findings, we detect a new realism about cyber-security readiness. Unsurprisingly,

the companies that are most advanced in their digital strategies are also the companies that

are putting the most effort into their cyber defences. That underscores a crucial point: like the

other aspects of digital transformation, cyber security provides an opportunity for forward-

thinking companies to differentiate themselves from their peers.

3Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

That differentiation will only grow in importance. So,

while the findings of our 2019 survey offer considerable

encouragement, they also throw down challenges for those

companies that are not yet prioritising digital engagement.

Leadership is of the utmost importance here. Although the

companies surveyed now have a specific person leading

their digital transformation, many have no formal training in

digital technology. That raises the question of whether they

have the capabilities to perform effectively in their role.

The greatest challenge for real estate companies is to

undertake the cultural shift required to attract and retain

the tech talent that will allow them to keep their digital

transformation on track. In this way, the 2019 KPMG survey

provides both a snapshot of today and a blueprint for

thefuture.

Andrew

Weir

Global Chair,

Real Estate &

Construction

Andy

Pyle

UK Head of

RealEstate

Sander

Grunewald

Global Lead,

RealEstate

Advisory

This paper is informed by a survey KPMG member

firms ran between July and August 2019. In its third

year and known as the PropTech Survey, it sought

opinions on digital transformation and technology

innovation from 188 real estate companies.

This covered companies from across the globe,

predominantly in the UK, continental Europe, the

Americas and Asia, and spanned a broad range of

subsectors and company sizes. The canvassing of

property firms was accompanied by a parallel survey

of 92PropTechcompanies.

4 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

10

Investment in digital,

IT and PropTech

collaboration is driven

by a need for improved

efficiencies (65%),

cost-reduction (47%)

and enhanced decision-

making (44%), rather than

increased revenues.

Barriers to further digitalisation include

unclear ROI (40%); digital not a priority

(40%); lack of a designated person to drive

the strategy (34%); and lack of appropriate

in-house talent (27%)

More likely than not (65%

of cases), it isn’t a digital or

technology specialist leading

digital transformation. 40%

of digital leaders come from

a real estate, construction or

finance background.

7 in 10 respondents are

confident in the cyber security

readiness of their organisation.

Digital strategies rarely incorporate

data management or a data strategy.

Only 25% of respondents have a

well-established data strategy that

enables the capture and analysis of

the right datasets. A third have no

data strategy at all.

Levels of system

integration are low –

overall, respondents rate

themselves as average,

5.4

out of

64%

of real estate companies have some

form of Property as a Service across

their portfolio and 13% are considering

it. Property as a Service still a small

proportion of overall space.

Asset management is the area most likely

(64% of respondents)

to benefit from

investment in IT,

digital technology or

PropTech collaboration

over the next 12

months.

Key survey findings

Real estate

companies are

increasingly

embracing

digital: 58% of

respondents have

a digital strategy in place, up from

52% in both 2018 and 2017.

95% of real estate companies

have someone responsible for leading

digital transformation and innovation.

In 62% of cases this is a senior

employee at a C-suite level or

equivalent.

5Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

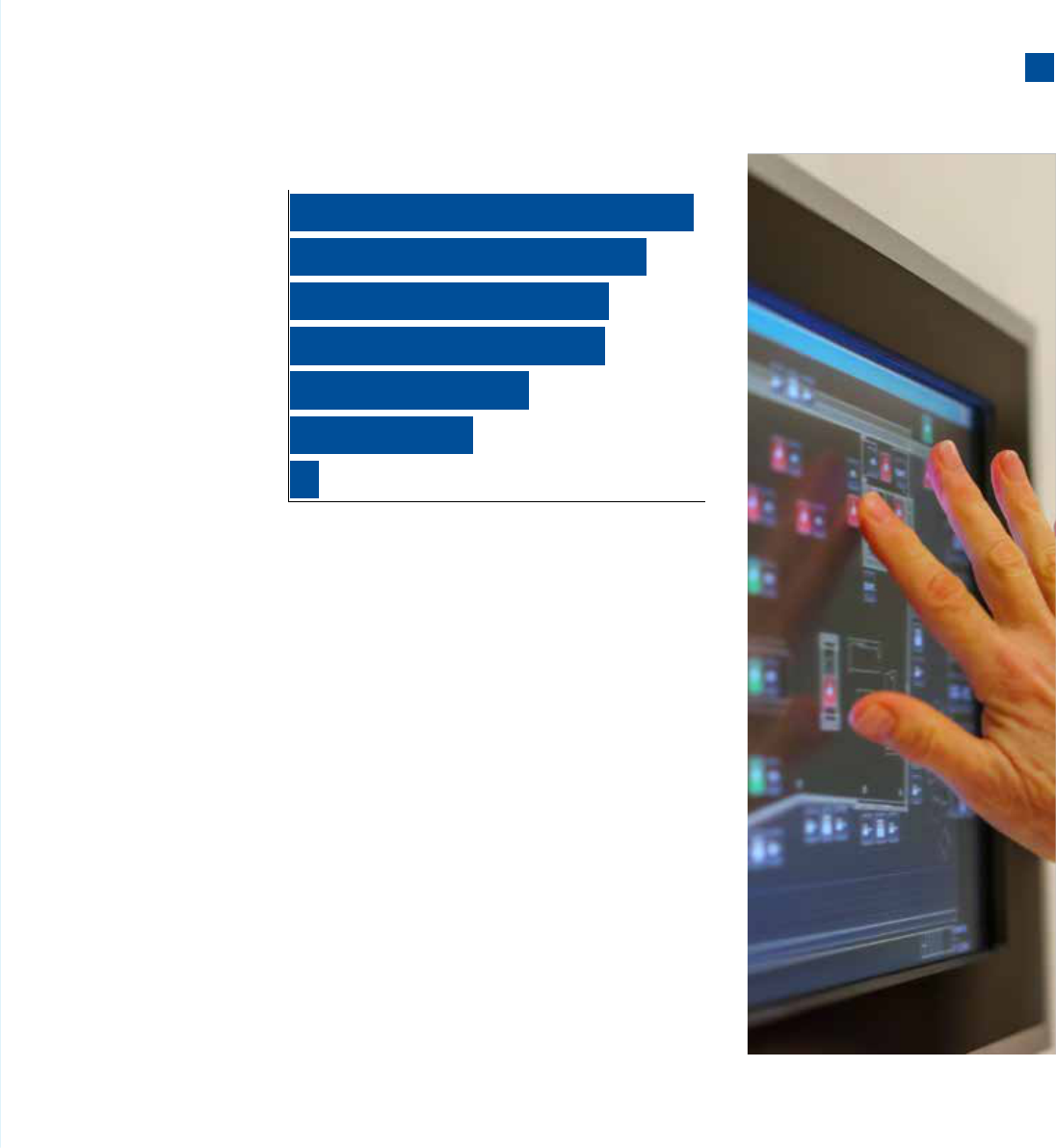

Extent to which property companies have a digital strategy

Growing engagement

with digital

Real estate companies are increasing their engagement with digital, and

most now have a specific person leading their digital transformation.

This is usually a senior employee. Enterprise-wide digital strategies are

not yet the norm, however, and a significant proportion of companies

still have no digital strategy at all.

The survey data indicates that adoption of

digital strategies is growing steadily. In this

year’s survey, 58% of respondents stated

that they had a digital strategy in place, either

enterprise-wide or within pockets (Fig 1.), up

from 52% in both 2018 and 2017.

Less than a third of respondents claim to have

an enterprise-wide digital strategy, however.

This might indicate that companies are

increasingly aware of the difficulties involved

in implementing an end-to-end strategy and

are therefore being more realistic in their

assessments than in previous years.

That finding is mirrored in the views of

PropTech respondents, who perceive that half

of property companies have a digital strategy

in some parts of the business, with 14%

having complete coverage and 28% with a

strategy in development. A fifth lack a strategy

altogether. What real estate companies say

and what PropTech respondents perceive

areconsistent.

In place

enterprise-wide

In some areas

In development

Do not have a

digital strategy

29%

23%

19%

29%

6 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

95%

of respondents have a

specific person leading

digital transformation

62%

of these are usually

a senior employee,

often at C-suite level

89%

this employee reports

directly to the owner, CEO,

president or board member

“More and more real estate

professionals are contacting

us about implementing

technology, and we are also

seeing increased interest in

creating a data strategy.”

Wouter Truffino – Founder, GlobalPropTech

The growing engagement with

digital has been accompanied by the

appointment of people to lead it. The

vast majority of 2019 respondents

(95%) have a specific person leading

digital transformation. Usually

(62%), this is a senior employee,

often at C-suite level. And in most

cases (89%), this employee reports

directly to the owner, CEO, president

or board member. This shows

that companies are taking digital

transformation seriously.

Only 10 of the 188 respondents do

not have someone responsible for

technology innovation and digital

transformation in their organisation.

The main reason given is that digital

transformation is not a business

priority for these companies.

Unsurprisingly, these companies

tend not to have a company-wide

digitalstrategy.

7Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Why companies

look to digital – and

where they dier

Real estate companies are pursuing digital investment

and collaborating with PropTechs for a variety of

reasons. For now, however, the focus is on improved

efficiencies and enhanced decision-making rather than

revenue generation or customer engagement.

Companies’ main objective in adopting digital is to improve

efficiencies and decision-making. This is confirmed by PropTech

respondents, who claim they’re normally brought in to do the

following: improve efficiencies (65% of the time), reduce costs

(47%) and improve decision-making (44%).

Business improvements PropTechs have been hired to deliver

in the last two years

Cost reduction

Help improve decision making

Help improve efficiencies

(speed as well as operational)

Help improve customer

engagement

Co-create new solutions

Help improve asset

performance

Help maximise revenue

Percentage selected

0% 10% 20% 30% 40% 50% 60% 70%

65%

47%

44%

40%

37%

33%

30%

8 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Objectives of past investments in IT, digital or Prop Tech collaboration

Revenue

maximisation

Improved

decision making

Improved asset

performance

Improved customer

engagement

Improved

effieciencies

Cost

reduction

Co-create new

solutions

Percentage selected

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

100%

Developement Asset Management Investing & financing

Past investment in IT, digital or

PropTech collaboration was also

intended to improve efficiencies

and decision-making (Fig 3).

This is consistent across three

of the property life cycles

we’ve explored in more detail:

development (by which we mean

design and planning; construction;

demolition and remediation),

asset/property management (fit-

out and refurbishment; sales and

leasing; property management)

and investment & financing

(asset acquisition and disposal;

valuations;financing).

Brokers and advisors in

thelead

The differences between types of

organisation are significant. Brokers

and advisors seem to be leading

the way over owner or developers

and property investors in almost all

aspects of digital transformation.

These include employing digital

experts to lead their transformation,

having an enterprise-wide

digital strategy in place, using

PropTech solutions and adopting

datastrategies.

Again, this result was backed up

by the PropTech responses. When

PropTechs were asked which

companies they saw as the most

innovative in the market, two of

the largest global brokers received

the highest number of unprompted

mentions. These were closely

followed by companies such as VTS

and WeWork.

This lead is most likely explained

by the highly competitive nature of

the real estate advisory industry.

To maintain their competitive

edge, companies are increasingly

using technology to differentiate

themselves. They have started to

invest in integrated systems, cloud-

based solutions, smart-building

technology and the automation of

the more manual aspects of their

businesses to free up their teams

to focus on value creation and

clientservice.

9Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Size matters too

Larger companies (those with more

than US$5 billion in assets) are

more likely to have an enterprise-

wide digital strategy in place. And

at larger companies, this strategy

is more likely to be led by someone

with a background in technology.

This is true of 44% of companies

with more than US$5 billion in

assets, compared with 21% of

those with US$1 billion to US$5

billion and a quarter of those with

less than US$1 billion. This may be

because the larger companies have

the resources to bring in skilled

personnel to own and lead digital

transformation.

Larger companies are also more

likely to have PropTech and digital

solutions seamlessly integrated

into their core IT systems.

Meanwhile, a full quarter of

companies under US$5 billion do

not have a digital and or technology

innovation strategy at all. This

compared with just 6% of those with

assets over US$5 billion.

This trend also applies to data

strategies and cyber security.

As detailed in further chapters,

companies with larger portfolios

have more resource to allocate to

thesefunctions.

Barriers to further engagement

What might be impeding further

engagement with digital? The

survey suggests that the main

factors are the skills gap and the real

estate industry’s culture of caution

andconservatism.

1. Skills

The skills gap was identified by

several of the PropTech companies

that responded to the survey. One

respondent put it thus:

“Property companies need to

be educated on the benefits of

using technology. They can often

get overwhelmed if they don’t

have a technical or digital role in

house which can take the lead on

theseprojects.”

Another respondent said that real

estate companies should “hire

experts who can take the business

forward. Run lots of different pilots

to experiment and learn. These

companies have to understand that

disruption in the industry will follow

and they should be better prepared to

survive the next decade”.

2. Culture

Culture is important here. Currently,

there is a cultural mismatch between

real estate – an industry that is

reluctant to let go of its traditional

practices – and the innovative,

“move fast and break things”

culture favoured by experts in digital

technology. The ‘dinosaur’ aspects of

the real estate industry may present

a considerable barrier to progress.

“Property companies need to

be educated on the benefits of

using technology. They can often

get overwhelmed if they don’t

have a technical or digital role in

house which can take the lead on

theseprojects.”

Survey respondent

10 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

PropTech companies noted the

need for real estate’s culture to

change. Companies should aim

to create and sustain a culture of

innovation that attracts people with

the right skills and enables them

to thrive. Employees need to feel

empowered to try out new ideas,

challenge the status quo and broker

new partnerships and collaborations

withPropTechs.

Employees also need to feel they

have the freedom to fail when

trying to innovate. One of the most

common themes in survey responses

from both property companies and

PropTechs was the importance

of experimenting more. And that

sentiment is echoed by other

industries, as uncovered in KPMG’s

CEO Outlook survey ran earlier this

year. Some 84% of CEOs said that

they wanted a culture in which errors

were accepted as part of the process

of innovation.

Of particular interest in the 2019

PropTech survey were the perceived

barriers to closer collaboration

between PropTech and property

companies, and the suggestions that

PropTech companies had for how

property companies could improve

their engagement with PropTech.

The barriers identified by the

PropTech companies included unclear

returns on investment (40%); not

being a business priority (40%); the

lack of a designated person to drive

the strategy (34%); and – importantly

– the lack of the appropriate talent at

property companies (27%).

Another barrier to collaboration is

the retention of talent at property

companies. According to the

PropTech companies, this leads to

regular re-treading of ground with

new hires.

40%

unclear returns on

investment

40%

not being a

business priority

34%

the lack of a

designated person

to drive the strategy

27%

the lack of the

appropriate talent at

property companies

11Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

“Developing a technology system is

something everyone tries to do internally

at first, believing if they build it in house,

they’ll have more control. This is a

mistake – the fact of the matter is we are

all running the same business systems,

slightly differently with different people.

Unless you are willing (and can afford) to

set up a dedicated team to maintain the

system, you should develop your proof

of concepts internally, then go out and

find best-of-breed solutions.”

Shen Chiu – Development Director – Investa

3. Absence of digital strategy

The lack of digital strategy in a fifth

of the companies engaging with

PropTech is another key finding. Are

these companies relying on PropTech

companies to guide them through

their digital transformation? There

is an opportunity here to encourage

companies to adopt a strategy before

engaging with PropTechs, so that

they can reap greater benefits from

the process. Most respondents said

that the main business sponsor of

PropTech initiatives at real estate

companies is usually the owner, CEO

or a board member, or another non-

digital person.

Recommendations to increase

PropTech collaboration

Many PropTech respondents

suggested changes that property

companies should consider

to increase engagement and

collaboration. These were the main

suggestions – which together provide

a roadmap for property companies’

digital journey:

• Creating new boards or

committees related to digital

transformation.

• Educating themselves on the

benefits and value of technology.

• Hiring experts who can take the

business forward; running pilots,

experimenting and learning.

• Ingraining digital transformation

into the culture of the business.

• Allocating budgets for digital and

PropTech collaboration; seeing

these as investments, not costs.

• Co-creating solutions.

Cooperating with peers on

digital roadmaps for property

companies. Providing sandbox

locations for PropTechs to

testsolutions.

• Distinguishing between genuine

PropTech companies and those

that are not; and assembling a

stable of providers accordingly.

• Streamlining the procurement

process for technology

companies to allow fast trials.

• Investing in start-ups or setting

up presences in incubators or

accelerator centres, to seek out

and fund PropTechs.

• Using fit-for-purpose applications

and staying away from

spreadsheets.

• Being more open about business

problems and challenges.

12 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Main driver for future investment in IT, digital and PropTech collaboration

Development Asset

Management

Investment &

financing

Percentage selected

Board/senior management priority Improved decision making

Improved asset performance

Reduced costs Improved customer engagement Improved efficiencies

Improved return on investment Other

0%

20%

40%

60%

80%

100%

22%

19%

3%

6%

14%

1%

31%

4%

19%

15%

11%

1%

18%

3%

13%

20%

20%

34%

7%

2%

2%

5%

23%

7%

As discussed above, real estate

companies’ main reasons for

investing in IT, digital and PropTech

collaboration have been to improve

efficiencies and decision-making

rather than to maximise revenue or

increase customer engagement. This

attitude has not yet shifted. As Fig.

4 above shows, the main drivers of

future investment in these areas are

still very much along the same lines,

along with prioritisation by the board

or senior management.

This suggests that real estate

companies are still missing at

least a couple of tricks. There’s a

telling contrast with the PropTech

companies, whose respondents put

heavy emphasis on their customer

engagement. And the disruptive

potential of digital is such that a

narrow focus on efficiencies rather

than opportunities is unlikely to be

helpful.

13Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Bridging the

skills gap

The survey shows that most of the people leading digital transformation at real estate

companies (65%) do not have a background in digital technology from outside the

industry. A significant number (40%) come from a real estate, construction or finance

background. This suggests that they may need additional professional development

to ensure they have the necessary capabilities to perform effectively in this role. In

general, we observe that talent and skills across the industry have evolved to serve the

market as it was, not as it might be in thefuture.

As discussed in the previous section, the skills gap was widely identified by PropTech respondents as a problem for real estate

companies. Given the cross-industry ‘war for talent’ – and the white-hot competition for digital, technology and data skills – real

estate companies need to up their game to attract the necessary capabilities. They can do this by investing in upskilling their

workforce or by fostering a culture of innovation that acts as a magnet for talent. Or they could do both.

Professional specialism

27%

Real estate or

construction

4%

Brokerage or sales

and marketing

10%

Strategy

30%

Technology

11%

Professional

services

5%

Data analystics

13%

Other (mainly

accounting &

finance)

14 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

“In the UK a number of property companies have been

recruiting from outside the industry to bring in the skills that

are needed in the future, whether data scientists, innovation

specialists or customer experience. As well as this, industry

bodies and universities will need to adapt their courses and

professional training so that the surveyors of the future are

equipped to deal with a digital future. Talent and skills is one

of the key workstreams for the British Property Federation’s

Technology & Innovation Working Group”

Andy Pyle – KPMG in the UK and Chair, British Property Federation Technology

&InnovationWorkingGroup

Upskilling the workforce appears

to be ranking higher in companies’

priorities. Of the CEOs who

responded to KPMG’s CEO Outlook

survey, 44% said that they were

intending to upskill more than half of

their current workforce in new digital

capabilities over the next three years.

But less than a third were prioritising

workforce investment over technology

investment. There is a danger in

real estate, as in other industries,

that companies will improve their

technology before ensuring that their

employees have the necessary skills

to employ iteffectively.

Regional variation is considerable.

UK respondents are more likely than

those from the rest of Europe and the

Americas to have a technology person

in charge of leading and managing

innovation and digital transformation.

Of UK respondents, 43% had a digital

expert here, compared with almost

a third in the rest of Europe and the

Americas and 20% in Asia and the

rest of the world.

In the Americas, the digital leader is

likely to be more senior, with 68%

being members of the C-suite. This

compares with 57% in the UK and

54% in the rest of Europe.

Also, Europe (excluding the

UK) is behind the curve when it

comes to hiring chief information

officers, chief digital officers and

chief technology officers to lead

digital engagement. Only 10% of

European respondents had done

this, compared with almost a fifth in

the UK, the Americas and Asia.

Clear patterns were also apparent by

sub-sector. Of brokers and advisors,

half have a digital expert leading

their technological innovation and

transformation, compared with 27%

of owners or developers and 39% of

property investors.

There is also a correlation between

having a digital strategy and having a

digital expert in charge of innovation

and digital transformation. Of the

companies with a company-wide

strategy, half had a digital expert in

charge of these areas, compared with

only a third of those with a strategy in

some areas of the company and just

11% of those with no strategy.

15Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Data strategy and

data protection

Companies have made relatively little progress in developing integrated digital

strategies that incorporate data management or a data strategy. Only a quarter of survey

respondents have a well-established data strategy that has enabled them to capture and

analyse the right datasets from across their portfolio of buildings for some time. And

almost a third have no data strategy at all. The conclusion must be that many companies

think they can have a digital strategy without a clear data strategy. KPMG member firms’

experience, however, is that data has to be at the heart of a broader digital strategy.

Meanwhile, data protection and cyber security are pressing issues that have yet to be

fully addressed by many companies.

This underscores the property industry’s

overall digital immaturity. Companies need

to spend more time identifying the problems

they can tackle through data, as well as the

data sets they need to capture and analyse to

deliver better customer outcomes.

The rise of ‘big data’ presents significant

challenges. The bulk of data available today

has been created very recently, and most

of it is ignored by companies. Today, all

businesses are faced with a situation in

which they may not be able to process all the

available data – or even identify the data that

would be most useful when processed. For

real estate companies, the first step must be

to capture the most valuable data to produce

insight and support decision-making.

Statements that best describes companies’ data strategy

Have a data strategy in place

and have been capturing

relevant data sets from across

our buildings for some time

Have devised a

strategy and recently

begun capturing data

from our buildings

Have a data strategy but have

not started capturing data

Don’t know

Do not have a

data strategy

28%

13%

29%

25%

5%

16 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

“Digital and data strategies are of no value if they

are not driven by clear customer (or operational)

outcomes. The term strategy can be frequently

misinterpreted as something broad and abstract that

applies to everything and everyone. Industries that are

embracing the digital and data age more often tend

to consider strategies in this way. Clients will often

say they have a strategy, but when we dig a bit deeper

they struggle to articulate or substantiate what it will

deliver for their customers. The best strategies are

the ones that start small, are customer-focused, are

repeatable and are scalable.”

Brendon Ambersley, KPMG in the UK

The effective capture of data

requires a data strategy. Of the 152

survey respondents with a digital

strategy in at least some areas or

in development, 76% had a data

strategy to some extent (Fig. 5).

This demonstrates a high crossover.

In cases where there isn’t a data

strategy, it’s typically because the

digital strategy is still in development.

This suggests that there is still a

long way to go in the process for

manyorganisations.

After data capture, the next challenge

is interpretation. At present, the

industry is confronted with a ‘data

chasm’, whereby the ability to make

use of data trails far behind the

amount of data available. Despite

predictions of greater investment in

future, just 10% of respondents have

data-led decision-making embedded

across the organisation and

supported by integrated infrastructure

for data visualisation (Fig. 6).

17Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

To cross the data chasm, companies

need the appropriate tools and

training, support (read data

ownership) from senior management

and improved production and

organisation of the data itself.

There are some positive signs,

however. The industry has started

looking at providing appropriate data

standards and mechanism for sharing

and managing data across the whole

lifecycle of a building. And there

are growing requests for standard-

setters, regulators, governments,

property companies and PropTechs

to come together to provide an

understanding of both current data

standards and the road ahead.

For many property companies,

the solution will come through

cooperation with companies

specialising in data. A senior

executive from Altera, a Dutch

provider of institutional real

estate funds, commented:

“We clearly see opportunities

in partnering with outsourced

parties in order to leverage all data

gatheredcollectively”.

Extent to which decision-making is led by data

Data-led decision making is embedded

across the organisation supported by an

integrated infrastructure for data visualisation

Data-led decision making within teams

supported by business analytics tools but

limited integration across functions

Structured approach to using data for

decision-making, but lacks governance and

supporting business analytics tools

Data is available in silos; usage is ad

hoc and team/ people-dependent

Not data-led, largely based on

group judgement/ intuition

Don’t know

Percentage selected

0% 10% 20% 30% 40%

10%

21%

21%

31%

11%

6%

“I see companies being more open source

and willing to engage with others in the

community than they have ever been.

This is a welcome development because

we go further when we work collectively

to create mutual success. […] What I am

really impressed about is that the industry

in Australia works together to develop

frameworks for how we will monitor and

respond to Cyber-security incidents”

Sheridan Ware – CIO – Charter Hall

18 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Two industry-specific challenges

are relevant here. The first is the

industry’s current lack of digital

leadership (as discussed earlier).

According to the KPMG/Harvey Nash

CIO survey, digital leaders view data

differently from their peers. They are

more likely to maximise the value of

the data they hold (35% vs 9%), and

they are more likely to maintain an

enterprise-wide data management

strategy (36% vs 10%).

So digital leaders in the property

industry should be aiming to get

data-driven insights that they

can trust and use to inform their

decision-making. They should also

aim to drive enterprise-wide data-

management strategies that focus on

theconsumer.

The second industry-specific

challenge is cultural. Companies

often overlook that data strategies

are more about cultural practices

than technology change. This

means influencing and changing

behaviour from being ‘system led’

to ‘data driven’.

How? By systematically identifying

opportunities where better outcomes

can be effected through better

data. Once the C-suite see and

believe the improved outcomes,

the behavioural changes will follow

from the top. Executive, operational

and digital leaders will be more

willing to subscribe to their new

roles and responsibilities with regard

to data. They will continue to drive

the improvements they have seen

and will replicate them across the

organisation. This should lead to the

dawn of a new culture.

19Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

With greater data capture comes

the need for greater data protection.

This is just one aspect of the broader

issuer of cyber security.

Over two-thirds (67%) of

respondents are either “quite

confident” or “very confident” of

their cyber security. This is in line

with the sentiment across other

industries – 68% of CEOs globally

say that their organisation is prepared

for a future cyber-attack (KPMG CEO

Outlook2019).

Some of this confidence may be

misplaced. As Altera observes, “You

can never be ‘very confident’ on the

area of cyber security.”

Somewhat surprisingly, more than a

fifth of respondents had undertaken

none of the five cyber-security

assessments we asked about in the

survey: cyber maturity assessment;

system/building penetration testing;

business continuity management in

case of breach; supplier security risk

management and data protection

under the European Union’s General

Data Protection Regulation.

Besides these assessments,

companies’ employees are also a

key line of defence and will require

investment in education and training

if data is to be as secure as possible.

Companies with digital strategies,

whether in place or in development,

were more confident of their cyber-

security readiness. So there is a clear

opportunity to show the benefits

of a digital strategy by linking it to

cybersecurity.

67%

of respondents are either “quite

confident” or “very confident”

of their cyber maturity

30%

have not tested

their preparedness.

Confidence in current cyber-security readiness

Not at all

confident

Not that

confident

Quite confident

Very confident

Don’t know

20%

48%

21%

7%

4%

20 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Cyber-security assessments undertaken

Business continuity management

in case of breach

Data protection under EU GDPR

System/ building penetration testing

Cyber Maturity Assessment

Supplier security risk management

None of these

Other

Percentage selected

0% 10% 20% 30% 40%

50%

48.6%

42.9%

38.4%

37.9%

28.8%

22.0%

3.4%

Of the potential assessments,

business continuity management in

case of breach was most commonly

performed (49%), followed by

data protection under EU GDPR

(43%), system/building penetration

testing (38%) and Cyber Maturity

Assessment (38%).

And while data testing under GDPR

had been undertaken by 70% of

European respondents, including

those in the UK, a full 30% have

not tested their preparedness.

Meanwhile, there are questions

over how well prepared American

respondents are to protect the data

of their European clients.

Importantly, cyber security shouldn’t

be seen as a purely defensive

capability. Instead, information

security should be viewed as a

strategic function and a source of

competitive advantage.

Transparency is crucial here. By being

forthcoming about how they handle

data and privacy – even to the extent

of showing how they deal with data

breaches – real estate companies can

differentiate their brands and foster

greater trust among consumers.

21Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Systems

integration: much

to be done

Levels of systems integration are low at present. Most

companies run different systems that are neither properly

integrated nor cloud-based and mobile-enabled. Very few

are using a single system to conduct all their operations.

We asked respondents to rate the integration of their internal systems

from 1 to 10. A score of 1 reflected a patchwork with no integration

while 10 represented fully integrated internal systems. The great

majority of respondents (85%) rated their systems between 3 and 8,

with 44% between 4 and 6. The mean score was 5.38.

In line with the findings on digital transformation, brokers and advisors

were the most advanced of the sub-sectors here. Property investors

and owners or developers were some way behind, as Fig.9 shows.

Extent to which decision-making is led by data

Systems integration – mean score

Below

average

Owners/

developers

Property

investors

Brokers/

advisors

Below

average

Highest

ranking

5.0 5.2 6.2

22 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

By company size, however, there

was little difference. The fairly

even distribution of scores by the

total amount of assets suggests

that size of business isn’t a major

factor in determining the level of

systemsintegration.

Extent to which decision-making is led by data

Systems integration – mean score

Businesses have a

digital strategy in place

across the business

Businesses have

a digital strategy

in some areas

Businesses have

a digital strategy

in development

6.2 4.8 5.6

Businesses do

not have a

digital strategy

4.5

A more telling factor was the

presence of a digital strategy – either

in place across the business or in

development. Perhaps unsurprisingly,

companies with business-spanning

digital strategies were likely to be

the most integrated, but those with a

digital strategy in only some areas did

flag that they were less integrated.

These companies had mean scores

closer to those with no strategy

indevelopment.

With a mean score of 5.73,

integration is more advanced

in Europe (excl. UK) than in the

Americas (5.09) or the UK (4.86). But

Asia and the rest of the world put

themselves highest, at 6.14.

KPMG’s anecdotal evidence suggests

that the average self-assessment of

5.38 is at best optimistic. Real estate

companies are still getting to grips

with their technical debt caused by

over a decade of underinvestment

in IT. According to our estimates, a

property manager or developer can

operate up to 30 standalone systems

to manage finances, operations and

different stages of the property value

chain (acquisition & construction,

marketing & sales, property

management, customer & facility

services, portfolio optimisation, etc.).

The lack of integration across

systems and functions results in

inefficiency, task duplication and,

most significantly, unreliable reporting

and several variations of the truth.

Fragmented IT infrastructure is

also making it very difficult for real

estate organisations to achieve

agility. The constraints of legacy

IT and the lack of collaboration

across organisational silos make

it impossible for companies to be

nimble and responsive to changes in

their environment. This is an issue

recognised by other industries – 79%

of CEOs responding to KPMG’s CEO

Outlook said they are responsible for

overseeing greater cross-functional

alignment in a way that their

predecessors were not.

Given these challenges, real estate

companies should undertake a

detailed mapping of their current

landscape of systems. This will allow

them to identify its shortcomings

and work out what a full-scale

transformation should achieve.

23Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

“PropTech is not seen as a priority for the

business which conducts itself on a ‘business

as usual’ basis. It’s seen as an opportunity

but also a cost. Excel dominates, as well as

experience or local knowledge.”

US real estate firm

In doing this, companies need to ask

themselves a number of questions.

How can they use system integration

to enable business agility? How

can they encourage their people to

embrace change? How can they get

more value from the data they have

across their functions and systems?

And how can they provide the insight

and control to oversee widespread

innovation and transformation?

Cloud technology will play an

important part in this process. Cloud-

based solutions address fragmented

digital infrastructures made up of

a range of bespoke, on-premise

computational infrastructure. The

cloud offers scaled capabilities and

advanced technologies that can

transform how work used to be

conducted via legacy IT. It can also

enable companies to exploit the

power of artificial intelligence and

data analytics to develop meaningful

insights. The resultant efficiencies

should allow firms to focus on other

opportunities across the value chain.

Extent to which decision-making is led by data

Yes, most or all

Yes, some

No

Don’t know

20%

52%

23%

5%

24 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Currently, three-quarters of

respondents have at least some

cloud-based and mobile-enabled

systems for capturing live data

(Fig. 11). This level of commitment

may not be enough to allow them

to reap the full benefits of this

technology,however.

A US real estate firm notes that

PropTech “is not seen as a priority for

the business which conducts itself on

a ‘business as usual’ basis. PropTech

is seen as an opportunity but also

a cost. Excel dominates, as well as

experience or localknowledge.”

Again, cultural issues are among

the biggest challenges here. The

industry’s prevailing attitude has been

“if it ain’t broke, don’t fix it”. This is

beginning to change as companies

face up to the risks of losing market

share to digital and web-based

challengers. But the incumbents

are still playing catch-up, and their

vulnerabilities are exacerbated by

years of underinvestment – where

there has been any investment at all.

The survey’s findings should serve

as a wake-up call to companies

that have yet to open their eyes to

the opportunities created by digital

integration and the potential for

market-share expansion.

“The built-environment-related

industries need more harmonised

data policies and universal cross-

industry digitalisation approaches

and methods for the digital

transformation to really kick

off. Now non-compatible siloes

and ancient ways of working

are prohibiting even the basic

digitalisation efforts.”

Finish real estate firm

25Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

The property life cycle: a

focus on asset management

Asset or property management is the stage

of the property life cycle most likely to have

received IT investment in the past two

years and is also the stage most likely to be

using PropTech. It is a priority for future IT

investment and the highest priority to invest

in PropTech solutions or digital innovation.

The survey asked several questions about the different stages of

the property life cycle. We defined these stages as follows:

Development:

design and planning; construction;

demolition and remediation

Asset/property management:

fit-out and refurbishment; sales and

leasing; property management

Investment and financing:

asset acquisition and disposal;

valuations; financing

26 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

The responses enabled us to identify

which companies were involved

with each of these stages. Of the

real estate companies we spoke

to, four-fifths are involved in asset

management, with seven in ten

involved in development and seven in

ten in investment and financing.

The asset/property-management

stage is currently attracting the

most attention from both real estate

and PropTech companies when it

comes to digitisation. This is largely

because it is seen as requiring more

resources and effort than other

stages in the cycle. According to 43%

of respondents, asset management

is the most resource-intensive

stage of the cycle, followed by

development (33%) and investment

and financing (18%). The tasks

involved in asset management tend

to be straightforward and repetitive,

making them ripe for automation. This

means that there’s a big opportunity

for efficiencies.

The focus on asset/property

management might also be driven

by the growing value of the market

that it represents. This has been

forecast to reach $22.04 billion

by 2023, according to research

company MarketsandMarkets.

The increase has been driven by a

growing appetite for the Property-

as-a-Service model, rapid growth in

property projects (and especially in

‘smart buildings’) and the proliferation

of PropTech firms that focus on

thisstage.

In the asset-management stage,

business processes are managed

offline using spreadsheets and

manual labour in 34% of cases, with

a fifth using PropTech solutions on

a standalone basis and almost as

many using digital solutions on a

standalone basis (Fig. 12). In 17% of

cases, PropTech or digital solutions

are seamlessly integrated into the

company’s core IT systems.

By contrast, development and

financing are more likely to rely on

manual processes than PropTech or

digital, as the chart below shows.

Business-process management across different stages of the life cycle

Development Asset

management

Investment &

financing

Percentage selected

They are largely managed offline, using

spreadsheets and manual labour

We have a PropTech solutions on a

stand-alone basis

We have a digital solution on a

stand-alone basis

Have a PropTech/ digital solution seamlessly integrated

into our core IT systems

Other Don’t know

0%

20%

40%

60%

80%

100%

54%

12%

16%

6%

7%

5%

34%

20%

18%

17%

7%

4%

58%

11%

13%

10%

6%

2%

27Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Unsurprisingly, companies that have a

full digital strategy are far more likely

to have PropTech or digital solutions

seamlessly integrated into their core

IT systems.

Not only is there already more use

of PropTech and digital in asset

management, but this stage is

also the highest priority for new

technological solutions. Of our real

estate respondents, 44% said that

asset management was their top

priority, compared with 27% for

investment and financing and 23%

for development (Fig. 13).

Broker and advisor companies are

almost as likely to prioritise PropTech

solutions or digital innovation in

investment and financing as in

asset management (50% compared

with 53%). This may be because

the digitalisation of their asset-

management business is already well

advanced – in line with the previous

finding that brokers and advisors

are the most likely to be managing

their processes through PropTech or

digitalalready.

Over the past two years, asset

management was the stage most

likely to have received investment in

IT, digital or PropTech collaboration

(84% of respondents). This was

split more or less evenly between

large investments (41%) and small

investments (43%). Although most

companies had also invested in

development and investment and

financing (72% for each), these

were more likely to have been small

ITinvestments.

Priority to use PropTech solutions or digital and innovation

Development Asset

management

Investment &

financing

Percentage selected

High priority

Medium priority Low priority

Don’t know

0%

20%

40%

60%

80%

100%

23%

50%

23%

4%

44%

35%

16%

5%

27%

35%

31%

7%

28 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Asset management is also the

stage of the property life cycle most

targeted by PropTech companies

– because that’s where real estate

companies need them most.

All stages of the cycle are highly

likely to benefit from investment in IT,

digital tech or PropTech collaboration

in the next few years. Some 64%

of real estate respondents thought

there would be investment in IT,

digital technology or PropTech

collaboration in asset management in

the next 12 months. For development

and investment and financing,

the figures were 59% and 45%,

respectively. Only 4% thought there

would be no investment in IT, digital

or PropTech collaboration in asset

management, although 10% said

they didn’t know (Fig. 15).

In development and asset

management, even companies

without a digital strategy believe

that they are likely to invest in IT,

digital tech or PropTech collaboration

over the next few years. As noted

earlier, the main motivation for this

investment is improved efficiency and

decision-making.

Stages of the property lifecycle targeted by PropTechs

Percentage selected

0% 10% 20% 30% 40% 50% 60%

55%

38%

33%

18%

Asset management: fit-out and refurbishment;

sales and leasing; property management

Investment and financing: asset acquisition

and disposal; valuations; financing

Other (specify)

Development: design and planning;

construction; demolition and remediation

Likelihood for the organisations to invest in IT, digital or PropTech

collaboration in the next few years

Development Asset

Management

Investment &

financing

Percentage selected

Yes, in the next 12 months

Not in next 12 months but in the next 5 years

No

Don’t know

0%

20%

40%

60%

80%

100%

59%

19%

7%

15%

65%

21%

4%

10%

45%

32%

12%

11%

29Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Property as a service

The survey shows a real estate industry that is opening up to new, technology-driven

business models, including Property as a Service (PaaS). Property as a Service (or Space

as a Service) is the model whereby customers buy a package of services that lets them

make best use of the space with the asset owner operating the building and incurring

all the related costs. This is a significant shift from the traditional lease where tenants

pay rent with a service charge on top to cover the costs of operating the building.

This is a significant market. If we look

at flexible/co-working workspaces

alone, the global market value is

estimated at around $26 billion, and

the number of coworking spaces is

expected to grow at an annual rate of

6% in the US and 13% elsewhere.

So how are property companies

responding to this opportunity? Most

survey respondents (64%) offer some

sort of PaaS (Fig. 16). This is more

pronounced among companies with a

digital strategy in place.

Despite its potential, however,

PaaS still accounts for only a small

proportion of space. Of the two-

thirds of companies with some PaaS

offering, half have it in 10% or less

of their space. This may because the

returns on investment are unclear,

or because the size of a company’s

portfolio does not warrant a large

proportion of PaaS.

Having a digital strategy is correlated

with owning PaaS operations. A

third of companies that have a digital

strategy across the company (35%)

or have one in some areas (34%)

own PaaS operations that they

runthemselves.

Approach to Property as a Service/Space as a Service

Own Property/ Living/

Space as a Service

operations that they run

themselves

Lease space to companies

that provide Property/ Living/

Space as a Service, e.g. the

likes of WeWork

Have Property/ Living/ Space as a

Service in their buildings, but outsource

its operation to a different organisation

Not something they

do or consider

Don’t own Property/

Living/ Space as a

Service operations

but are considering it

Don’t know

28%

22%

14%

13%

15%

8%

30 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

“Improved customer engagement

is where we see a difference will be

made in the future”

Altera

The widespread adoption of PaaS is

an acknowledgement of the need

to become more customer-centric.

Nevertheless, when it comes to

prioritising IT investment, a focus

on the customer is outranked

by concerns such as improving

efficiencies, decision-making and

asset performance.

This contrasts starkly with practices

in PropTech, where most companies

invest in NPS scoring and place

great importance on customer

feedback and improving engagement.

According to one PropTech

respondent, “literally everything is

driven by feedback”.

For real estate companies, then,

there is still ample room for

improvement in the adoption of a

service model. As Dutch property

firm Altera says, “improved customer

engagement is where we see a

difference will be made in the future”.

31Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

The road

ahead

So what is the direction of travel in the coming

years? The survey suggests a rapid acceleration in

digital disruption – one that will demand urgent

cultural change from real estate companies.

The PropTechs are hugely optimistic about the growth of

their market. Of the PropTech respondents to the survey,

87% believe that the real estate companies they work with

will increase spending on PropTech solutions in the next 12

months. No PropTech respondents expect investment to

halt or decrease.

In the next two years, the PropTechs expect significant

digital disruption in a number of areas. Real-time asset

performance data was the area that the largest number

of PropTech respondents (25%) saw as most ripe for

disruption, followed by building optimisation (22%),

transactions (19%) and customer data (16%).

32 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

The PropTechs also see data capture

and management as one of the areas

where real estate companies are

currently least prepared. It’s clear

from the survey, however, that a lot

of real estate companies are working

on their digital strategies and are

also thinking about how they use and

capture data.

Equally, much work remains to be

done. Education and increased

awareness of digital opportunities

and threats are required to break the

resistance of senior decision-makers.

And companies need to get their data

right before they engage in PropTech

collaborations. That will entail

investing in mature systems and

processes for capturing, managing

and analysing data that can be easily

shared between applications.

It’s also unhelpful for companies

to be innovating in isolation.

Collaboration is essential, and there’s

a need for industry-wide standards

or common approaches for data

management and digitalisation.

Above all, the industry’s mindset

needs to change. Currently, many

property companies want digital

solutions but aren’t prepared to

budget for them. These companies

are insufficiently focused on the

opportunity to improve customer

service, and they are too nervous

about the risks of digital investment.

Instead, they should see digital

transformation as an opportunity

to experiment more and learn from

the results. For many, the first

step should be bringing aboard the

appropriate expertise – to ensure

that their digital future is in the

right hands – and then developing a

strategy forsuccess.

After that, the way forward will

involve starting small, experimenting

with innovations and becoming more

agile in the process. In a fast-moving

future, this agility will be essential

forsurvival.

“If you don’t use data efficiently and effectively

then you will miss a huge amount of value in

your business/market. Others will not make

this mistake and you will become increasingly

uncompetitive. Ultimately the world is only

going one way.”

UK REIT

33Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

About this survey

In July and August 2019, KPMG

professionals and research

organisation 3GEM sought opinions

on digital transformation and

technology innovation from 188 real

estate companies for KPMG’s third

annual PropTech survey.

This covered companies from across

the globe, predominantly in the UK,

continental Europe, the Americas and

Asia, and spanned a broad range of

subsectors and company sizes. The

canvassing of property companies was

accompanied by a parallel survey of 92

PropTech companies.

The survey tested companies’ digital

maturity and explored their views on

issues such as data-management

practices, cyber security, PaaS and

system integration.

The charts show the breakdown of

respondents by organisation type, asset

size, property type and geography.

Type of property they manage/own/invest in

Office (incl co-working & flexible working

Industrial & logistics (flex, warehouse)

Retail

Hospitality (hotels & other)

Residential (build-to-rent / multi-family)

Retirement & senior living

Student accommodation

Other

70%

65%

48%

19%

55%

22%

29%

20%

34 Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

Type of real estate organisation

Property investor, such as listed

or private firm, sovereign wealth

fund or fund manager

Property owner/

developer

Other

Broker/ advisor

48%

30%

13%

9%

Value of assets owner or managed

36%

29%

28%

7%

< US$1bn

US$1bn - US$5bn

> US$5bn

Don’t

know

Region where they are headquartered

16%36%

48%

Asia & rest of

the world

Americas

Europe

35Global PropTech Survey 2019

© 2019 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of

the KPMG network are affiliated. All rights reserved.

June 2019

kpmg.com/realestate

Contact us

Andrew Weir

Global Chair,

Real Estate & Construction

KPMG International

+852 2826 7243

andrew[email protected]

Andy Pyle

Head of Real Estate,

KPMG in the UK

+44 20 7311 6499

Sander Grunewald

Global Lead,

Real Estate Advisory

KPMG International

+31 206 568 447

grune[email protected]

kpmg.com

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity.

Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date

it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice

after a thorough examination of the particular situation.

© 2019 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms

are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind

KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any

member firm. All rights reserved.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Designed by CREATE | October 2019 | CRT118431B